CPF rejects application of 56-year old heart patient to withdraw from his CPF account, saying he is 'not physically incapacitated'

"I didn't ask for government welfare. I just want to take out my own money and save myself. I feel so helpless. What happened to the Singapore government?"

Mr Sim Kay Chuan, a 56-year-old Singaporean who suffered from heart problems in 2015 had an operation two years ago, leaving his heart’s left ventricular ejection fraction (LVEF) at 37% performance. The normal LVEF for a person ranges from 55% to 70%.

This condition left Mr Sim weak. On top of that, the medicine that he has to take also lowers his blood pressure, making him susceptible to fainting spells even when walking.

Mr Sim has since exhausted his savings as he is unable to work due to his medical condition for the past two years. That’s why he applied to withdraw his CPF to ease his family expenses.

However, the authorities refused his application on the grounds that he did not qualify, citing four conditions.

According to the official website of the CPF Board, in order to apply to withdraw some of your CPF savings on medical grounds, they need to certify that you:

- are physically or mentally incapacitated from ever continuing in any employment; or

- have a severely impaired life expectancy; or

- lack capacity within the meaning of Section 4 of the Mental Capacity Act (MCA) and the lack of capacity is likely to be permanent; or

- are terminally ill.

According to Mr Sim, he started to experience physical health problems since 2014. It was only until when he almost fainted after crossing an overbridge that he visited a Chinese traditional physician and was advised to seek treatment in hospital.

After examination in a hospital, Mr Sim was told that his heart is failing and he needed surgery.

Mr Sim underwent the surgery as advised. He was then told by the attending doctor that he is not to carry any weight more than 5kg and that he would not able to work for a long time.

In the two years since his operation, Mr Sim has tried applying for work but failed to secure any employment due to his medical condition. He could not take up jobs such as private hire driver either because of his tendency to feel giddy and possibly lose consciousness.

Currently, his wife is the sole breadwinner. She works as a welfare coordinator and earns a take-home pay of S$1,800. According to Mr Sim, their savings have been exhausted due to his medical treatments and medicines to lower his blood cholesterol.

Considered divorce to ease his wife's burden

He is worried about the family’s current financial conditions and even thought about divorce to avoid burdening his wife further. His wife refused to do so and believes that they should cherish and take care of each other.

Mr Sim's wife has to wake up as early as 5am, spend three hours on commute and work for nine hours each day. Besides paying the monthly expenses, she also gives her husband S$20-30 as daily pocket money.

At Mr Sim’s flat in Jurong, his wife showed TOC stacks of pawn tickets for jewellery which she had pawned, one by one for hundreds of dollars, in order to pay for medical bills and other expenses over the past two years.

Desperate in his current situation, Mr Sim resorted to applying for early withdrawal of his CPF monies which is now kept in the retirement account.

CPF states Mr Sim can still work and SSO states wife can provide for family

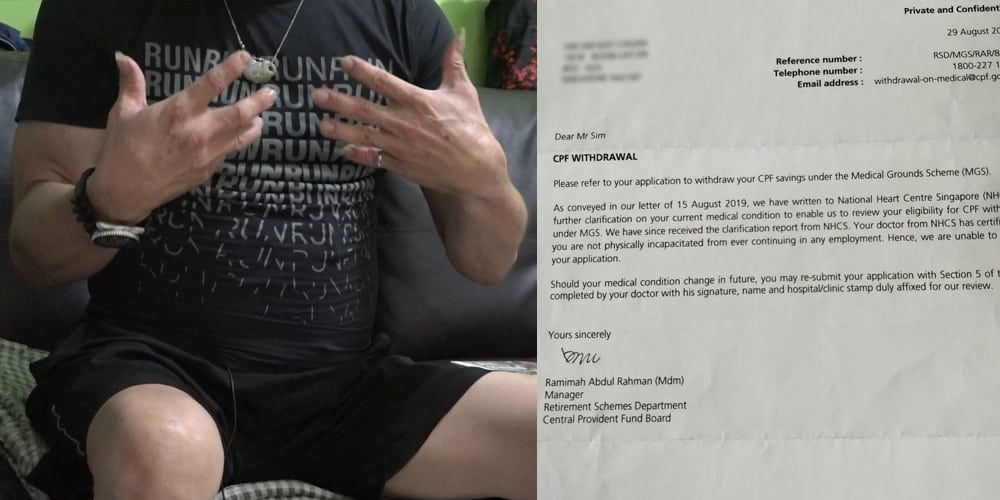

However, CPF Board in its letter to Mr Sim dated in August this year, said that after checking with the doctor, Mr Sim is “not physically incapacitated from ever continuing in any employment” (emphasis ours), and therefore they are unable to process his application to withdraw his CPF Retirement sum of around $18,000.

When Mr Sim visited Mr Patrick Tay, MP for West Coast GRC, other than writing an appeal to the CPF board, his case was also referred to the Social Service Office (SSO).

According to SSO’s letter from the Social Welfare Department dated 27 May 2019, his application for financial assistance was rejected on the basis that his wife was still working with a stable income. It wrote, "after careful consideration, we assessed that your family is able to support its basic living expenses."

There was no follow-up letter from the CPF Board other than a phone call to Mr Sim to saying that they found nothing wrong with his medical condition, once again rejecting his application.

So right now, Mr Sim can only start drawing from his CPF retirement account in another nine years when he turns 65. And according to him, he will only be able to withdraw about S$250 each month.

Mr Sim’s story was reported on by local Chinese press Shin Min daily last month.

Regret going for his heart surgery

The rejection by the CPF Board and the SSO made Mr Sim feel helpless, leading him to question why his own money cannot be used when he needs it the most. This is especially since he has no idea how long he has left to live due to his heart condition.

“I regret going for the surgery,” said Mr Sim.

“Ended up spending so much money and now becoming a burden for my wife. A couple of my friends who are in similar situation as me, share my thoughts.”

He went on to state that he does not want to depend on the government for hand-outs. Instead, he just wants to get his hard-earned money so that he can live with dignity and not rely on his wife for hand-outs.

Mr Sim also voiced out against the government's narrative that old men would go Batam and spend all their money there, "How can you use the stories of a few individuals as a reason to restrict the use of people's money?"

Sold HDB seven years ago

TOC had written to CPF board for their comments on this story in September and October this year but has not received any acknowledgement or reply till date.

Just in case CPF decides to disclose private information about Mr Sim and his wife as they had in the past with other families, we have to note that the couple is currently living in a BTO which they purchased five years ago. Prior to that, they lived in a rental flat for around two years after selling their previous flat for around $200,000.

When asked what they did with the money, Mr Sim shared that he had tried to dabble in business but failed. Part of the money was used to pay off debts which wife had incurred when borrowing money to pay for her mother’s medical fees and also for the flat that they are currently staying in.

The couple have a daughter, but when asked about her, they said she has her own expenses and family to look after.