Current Affairs

SDP’s Dr Paul Tambyah responds to the proposed amendments of MediShield Life

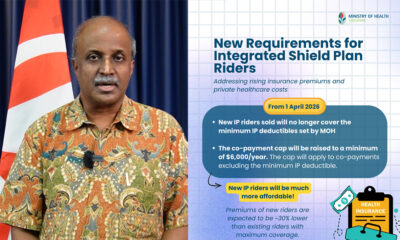

Previously on 29 September, the Ministry of Health had released a press statement on its website, inviting Singaporeans to their suggestions on the increase of MediShield Life premiums.

In response to the public consultation, Dr Paul Tambyah, the Chairman of Singapore Democratic Party (SDP) had contributed his views on the proposed amendments to MediShield Life.

Dr Tambyah pointed out that MediShield Life only covers “a small proportion” of the total healthcare cost in Singapore. He provided an example in 2018 when MediShield Life paid out close to S$1 billion out of a total healthcare expenditure of around S$18 billion.

Despite welcoming the fact that the costs of hospital treatments associated with substance abuse and suicide attempts will be subsidised, the SDP Chairman questioned the reason behind psychiatric treatment being paid for at a much lower rate than other kinds of medical conditions.

He added that this move singles out one category of illness, contributing to the stigmatization against those affected by mental illness in Singapore.

Furthermore, Dr Tambyah mentioned the caps on annual payments, daily payments, as well as the payments for various procedures like radiotherapy or day surgery.

Such cappings that are unique among national health insurance plans which usually cap the amount that an individual has to pay rather than the amount that the insurance covers.

“Under Medishield Life, someone with a serious illness that costs more than $150,000 a year has to find other funding to pay the balance of the costs.”

“Furthermore, these caps also do not take advantage of the fact that the government (through MOH holdings) is by far the largest provider of acute inpatient healthcare services which take up the bulk of costs.”

Noting that the improved benefits and reduced deductibles appear to be funded largely by the increased premiums, he revealed that the Medical Loss Ratios for MediShield Life are by far the lowest of any public mandatory health insurance scheme worldwide.

The Medical Loss Ratios are reported to be as low as S$3.5 billion out of S$7.6 billion collected paid out in the last five years.

Dr Tambyah criticised the argument used to justify the huge reserve requirement is to set aside to support future commitments like “long-term treatments and future premium rebates”, saying how it would not make sense if the premiums are set to increase every few years.

“Long-term treatments would also have been factored into the actuarial calculations which have not been made public. While some degree of “front-loading” may have been justifiable in the early years of Medishield Life when a number of individuals with pre-existing conditions previously excluded from Medishield are included for the first time. However, that number is unlikely to be repeated again.”

Lastly, the SDP Chairman talked about how the 3M structure (Medisave, MediShield and Medifund) with CareShield Life is “too complicated” which involved “significant administration and distribution costs”.

He suggested that the “most logical” approach to solve this issue is to replace the whole scheme with a single-payer national health insurance scheme.

“This is a simple sustainable plan which has the government manage a national health investment fund with contributions by the public based on taxable income. This provides basic health, accident and pregnancy coverage for all citizens.”

“There will be caps on the amount paid by the public and a return to the Singapore Medical Association’s fee guideline structure to cover more than just surgical procedures and institutions as well as providers.”

Dr Tambyah added that both the public and private sectors will be treated the same in terms of standards expected as well as the reimbursement according to SMA’s fee guideline.

“Evidence-based healthcare will be funded with small co-payments and the public and private sectors will be treated the same in terms of standards expected and reimbursement according to the fee guideline. The basic overriding principle is that the health of the people is paramount, not the profitability of the fund.”