Commentaries

IPS-TW analysis on CPF – unaddressed issue of retirement adequacy

The research team – Mark Whatley (Towers Watson, Singapore), Christopher Gee (Institute of Policy Studies) and Peter Ryan-Kane (Towers Watson, Hong Kong).

It is important to understand that, when the Institute of Policy Studies (IPS) and Towers Watson (TW) jointly published the paper on the investment risk on Singapore’s retirement financing scheme, there is actually a lot more that the paper does not say than what it professes to affirm.

Let’s start, however, with the one thing that the paper make no qualms about claiming. Through extensive evaluation and comparison with other investment plans, the IPS-Towers Watson team proposed that the average Singaporean is better off leaving money with the Central Provident Fund (CPF) rather than park it in other forms of investment.

This analysis was evidently made to debunk some claims that the team noticed in “online commentary” that suggested CPF members might be short-changed on interest rates, and that better returns might be had if they were to invest their retirement funds in other portfolios, such as in government bonds.

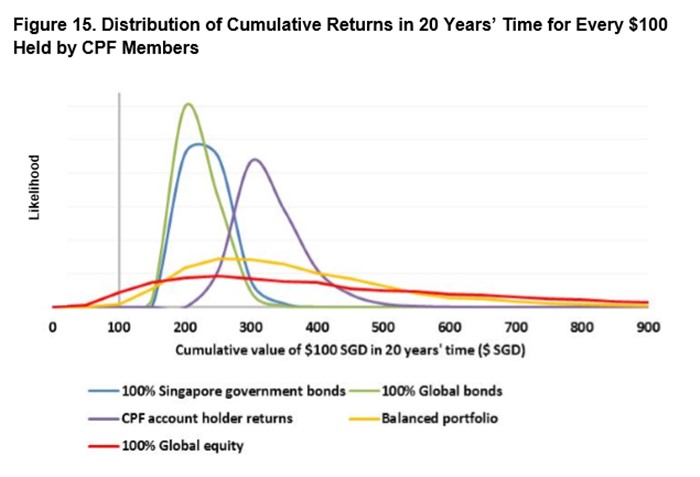

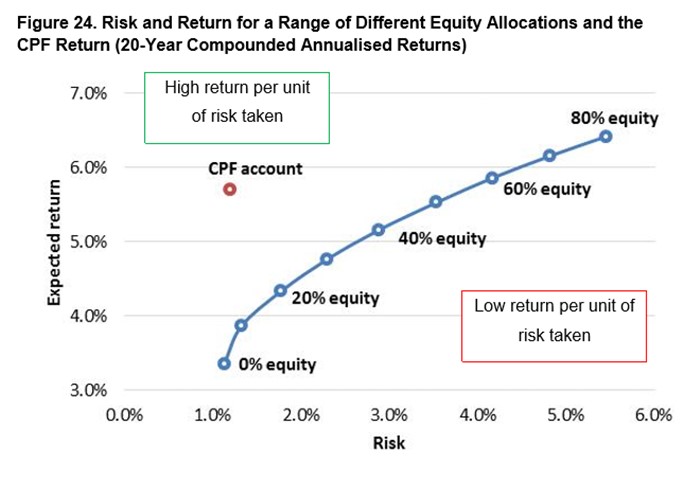

TW’s analysis, based on the company’s historical data, is that this is hardly true, as their calculations indicated that, over a long duration of 20 years (easily what CPF members would see as the point of “maturity” of their portfolio), the CPF system presents moderately high level of returns with minimally risk, which compares favourably to other investment schemes.

CPF returns compared to other investment portfolios, and the likelihood of its performance. (Image – IPS-TW paper)

CPF’s risk-return quotients, as compared to other forms of investment. (Image – IPS-TW)

Indeed, the returns offered by to CPF members through their Ordinary, Special and Retirement Accounts altogether make for a good investment portfolio, indicates the report. This is because the Singapore government effectively guarantees the rates offered to these accounts. Compared to other investment schemes, while not outstanding in the short term, these interest rates end up more profitable in the longer term.

“Our paper finds that the low-risk, very stable returns offered by the CPF are attractive as compared to those that may be generated by investing in a portfolio of 60% equities, 40% bonds – what we have termed a balanced portfolio that an independent financial advisor may recommend to an investor seeking a reasonable risk-return trade-off,” said Mr Peter Ryan-Kane, TW’s head of portfolio advisory in Asia Pacific. “On a 20-year view, based on a reasonable set of assumptions, the average CPF member is simulated to generate returns similar to this balanced portfolio, but would be exposed to significantly less risk.”

Now, we have no reason to doubt TW. The company has extensive experience in the study of investments and have the historical data to back up their claims. Yet, before the good people at the CPF Board give themselves a huge pat on the back for such a wonderful scheme and a year-end bonus to boot, the IPS-WT report must be put in perspective.

So long as the money stays in the account…

First, the study focused mainly on the accumulation phase, not the “decumulation” phase or withdrawals. In other words, the study assumes that, if a CPF member has money in the various accounts, it will grow positively. It does not consider the rather real and bleak situation that some might not even have money in their CPF accounts, for reasons ranging from paying for housing, healthcare, education, other forms of investment under the CPF Investment Scheme, or even loss of income.

And that is actually the key issue of the CPF system that we have today – that it is being used up for other purposes that undercut its ability to serve as an effective retirement nest egg. Nevertheless, retirement adequacy was not on the team’s charter for the report.

“We have not considered withdrawals for various purposes in this paper, because these withdrawals expose the CPF member to significantly different risk and return profiles that are extremely complex,” said Mr Christopher Gee, research fellow at IPS. “For withdrawals made from CPF for housing for instance, the risks/returns that a member is exposed to cannot be readily compared with the investment returns generated within the CPF or through market returns – for example, a balanced 60:40 portfolio.”

Can we expect a better analysis on this, given that housing is one of the key drains to CPF members’ accounts? “We have described some of these housing investment risks in the paper, and we contemplate looking further into the housing withdrawal issue in our follow-on research,” said Mr Gee.

So long as it stays under SSGS and current policies…

It is also worth noting that the rates that are “guaranteed” for all CPF account holders come about because of “CPF assets are for the most part invested in Special Singapore Government Securities (SSGS)”. The team has described this to be one of the key reasons why CPF members are participating in a low-risk retirement fund, although the dotted-line link to GIC Pte Ltd, an organisation shrouded in opacity, would give some very little assurance.

“CPF funds are not managed by GIC,” said Mr Gee. “CPF funds are invested in SSGS – which are essentially IOUs issued by the government – that pay interest at rates pegged to those payable into CPF members’ OA and SMRA. The proceeds from the SSGS are combined with other funds from the issue of standard Singapore Government Securities, and placed with the Monetary Authority of Singapore together with other government assets. Periodically, transfers are made from all of these co-mingled funds to the GIC to invest for the long-term. Because of the government’s other assets, Singapore’s credit standing is assessed amongst the highest in the world.”

“The way in which the GIC manages its funds is therefore a separate matter of overall governance and its responsibility to its client, the Singapore government,” said Mr Gee.

Notably, in taking this position, the team would not be addressing the various “online commentaries” that suggest CPF funds might have been lost in toxic investment made by GIC.

“It is not part of the scope of this paper to assess the management of assets at any Singapore Government entity,” said Mr Ryan-Kane.

Concern more pressing than “assured” returns

In effect, the report paints a positive outlook for CPF as a retirement fund, but the reality of the situation for the average CPF member is very different, who actively make withdrawals on CPF accounts for a variety of things. For the bulk of citizens, most of these withdrawals is to pay for the roof currently over our heads, rather than in property as any form of “investment”.

The IPS-TW paper might actually a say a lot about how CPF performs as an investment fund, but very little in how it performs as a retirement fund. The positive projections are still too ideal for the man on the street, who would likely experience a very different set of issues, including job security (which determines fund accumulation) and rising cost of living (which determines fund “decumulation”).

So while the IPS-TW might have satisfied “online commentary” that suggests our money can grow better if parked elsewhere – which also assumes that SSGS would not turn toxic on us for any reason, and if so that the government will continue to underwrite any such loss – what matters more to the average CPF member is the adequacy of CPF to see us through to the end of life. That is actually more telling of the effectiveness of the CPF system, which this paper has not made a point to address, nor is it expected to.

Notice: We now publish our news at The Online Citizen and Heidoh.