Aloysius Foo

A Temasek wrapped up in a mystery within the abyss of the Singapore economy

Public displeasure should be directed correctly, for it to be effective. The recent revelation, that Temasek Holdings has lost 31 percent of its net portfolio value between March and November 2008, is initially shocking, given its supposed reputation as a professional and long-term investor. Temasek also seemed to have made a wrong judgement on hindsight, when it injected capital into Barclays and Merrill Lynch.

Public displeasure should be directed correctly, for it to be effective. The recent revelation, that Temasek Holdings has lost 31 percent of its net portfolio value between March and November 2008, is initially shocking, given its supposed reputation as a professional and long-term investor. Temasek also seemed to have made a wrong judgement on hindsight, when it injected capital into Barclays and Merrill Lynch.

Understandably, especially during this recession, Singaporeans are concerned about Temasek’s performance. It is for a very good reason; Singaporeans believe they have a share in Temasek’s money through the sole shareholder, the Ministry of Finance.

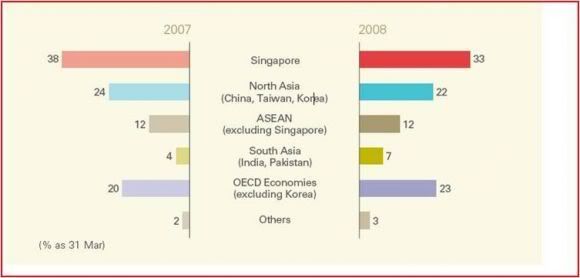

Firstly, Temasek’s performance is not very shocking if market indices elsewhere are examined. Temasek parks a third of its investments in Singapore, holds stakes in 7 out of the 10 largest companies here, and nests another 22 percent of its portfolio in China, South Korea and Taiwan. A sizeable chunk is also held in OECD economies (see below). As the name ‘Holdings’ implies, Temasek owns stocks in companies, and they don’t keep tonnes of cash in its drawers.

Figure 1: Temasek’s investment portfolio by geography (Source: Temasek Review 2008)

Figure 2: Performance of major market indices (Source)

Hence when markets fall, it is not surprising to see the value of Temasek’s portfolio falling as well. The figure above shows major global stock indexes – nearly all of them have dropped more than 30 percent in 2008, with some losing more than 40 percent. The (not shown in figure) MSCI (Singapore) and MSCI (Asia ex-Japan) stock indices are good benchmarks for Temasek’s performance: 31 percent loss against the 44 and 45 percentage losses suffered respectively. Furthermore, Temasek’s drop “is exactly in line with the MSCI world share index”.

Temasek is also not the only ‘sovereign wealth fund (SWF)’ to lose money. According to The Economist’s report on 22 January this year, “Gulf foreign-reserve funds and SWFs (the distinction is often blurry) lost $350 billion last year, or 27% of the value of their assets”. Though Temasek has failed to produce results, it has not failed spectacularly, giving assurance to the public their money has not been squandered away. In fact a 31-point loss is arguably a better performance, given the context of the market.

Finally, Temasek is not plagued with structural financial problems. While it may have bled money in Barclays and Merrill Lynch, and also encountered problems with Shin Corp and the Indonesian government, it has made other sound investments too, such as in the Bank of China and China Construction Bank. Its losses are likely to be reversed once the recession ends, the banking system is fixed, and investors are once again confident in the markets. Public anger directed at Temasek over its losses, if any, is unreasonable – Temasek is not an immediate failure.

Pointing your concern to the right way

While the Western financial world fears an onslaught of SWFs with hidden agendas, Singaporeans fear that Temasek has skeletons in its closets. There are three broad categories of problems which Singaporeans can express some reasonable suspicions: Temasek’s lack of transparency, soundness of its investment strategy and Temasek’s relationship with the giant local companies here.

The first problem is a recurrent theme. A recent Wall Street Journal article summed it up nicely –

“it has never provided historical financials to back up its claim of an 18% compounded annual “total shareholder return” by “market value,” nor has it released detailed results showing how money flows among its subsidiaries, the holding company and its government shareholder. Temasek outlines its compensation arrangements but doesn’t say how much it pays its top executives”.

What is the definition of ‘transparency’? Should Temasek publish its consolidated financial report like any other listed company, not just its summary – which is already quite detailed in stating its goals and investments? What stuff do Singaporeans want to see which is not publicly available?

The essence of this transparency issue is not regarding Temasek’s financial status, but more on its vague goals and the perception that it is a government-run body.

Temasek should be transparent for its own good – a pragmatic and financial purpose. Together with the GIC, they can detail their internal workings, goals and strategies to create a force of certainty and stability in the financial market. If Temasek, for no known reason, decides to give up its stake in a company, it will lead to speculations, rumours and uncalled panic, and Temasek will eventually be affected. More importantly, political tensions can be reduced in sensitive investments, as it has learnt in Thailand. Surely such benefits of transparency can better achieve its bureaucratically-crafted goal, “maximise long-term shareholder value as an active investor and shareholder of successful enterprises”?

The second problem is the soundness of Temasek’s investment strategy. Some have criticised it for pursuing a ‘high-risk strategy’, and so expose Singaporeans’ money to unnecessary losses. Temasek is not a low- or high-risk investor. Stashing money in fixed deposits or bonds are safe, but may not secure high returns. Similarly, pumping money into hedge funds or real estate speculation may offer higher returns, but Temasek is unlikely to be doing that. It is more likely Temasek is a mid-risk investor which made some bad decisions in Barclays and Merrill Lynch (Temasek’s losses cannot be fully attributed to just these two banks; as mentioned, it depends on the performance of stock markets worldwide).

Temasek holds stakes in companies in diverse sectors, ranging from financial services to consumer lifestyle to technology. Critics will jump at this again, arguing that diversification ought to act as a shock-absorber. However, 2008 was an unprecedented year where everything seemed to be going downhill. Even diversification may not work in such exceptional times, when confidence level is zilch in the market; but it will probably work once the economy recovers.

With the appointment of Charles Goodyear as chief executive, it looks set to diversify into asset classes such as commodities, where he has had experience. Benefit of the doubt can be extended to Temasek over its investment strategy, and Singaporeans need not be anxious that aggressive, high-risk investments will bleed them.

The third problem is the consistent link drawn between Temasek and companies where it is a stakeholder. Singapore’s commanding heights – the telecommunications, energy, industrial, transport and banking sectors – are anchored by local firms such as Singtel, Mediacorp, Singapore Power, SembCorp, PSA, SMRT and DBS. Some of these local firms were originally owned by the Singapore government to stimulate the growth of new industries, which then cut a route for private capital once viability was shown. As the economy grew, the government transferred part or all shares to Temasek, which is supposed to be an investment manager for the Ministry of Finance.

Temasek has stated clearly it is not involved in the commercial running of its companies. The evidence suggests so: in 2002, a battle was fought between DBS and 98 Holdings for NatSteel. Though Temasek owned shares in all three firms, there is no evidence to show it was the puppet master of this saga. Furthermore, Temasek firms such as SembCorp and Keppel compete actively against each other in their respective fields. Yet there are lingering doubts, especially when one of Temasek’s ‘investment themes’ is to ‘deepen comparative advantage’ – one can guess it means the ‘national champions’.

Most importantly, there is a perception the government directs Temasek in their investment ventures. Temasek and GIC are 5th schedule companies – their CEO and board members are appointed by the President (but this can be override by two-thirds majority in Parliament, which is not difficult to do so). Most people believe that because Temasek reports to the executive, it is likely to carry out its orders. This image problem has been compounded by Temasek’s lack of transparency.

Some Singaporeans are quick to jump at this – shadowy and subtle strokes to manipulate the economy behind the curtain, all in the aim of entrenching political dominance. Secondly, critics of local firms claim they crowd out small players. What is more significant is that the image problem may deter foreign partnerships or takeovers, limiting the growth of local firms.

The abyss of the Singapore economy

Some of these worries are unfounded. For a start, claims that Temasek-linked/Government-linked companies crowd out small players may be false. Mediacorp, PSA are natural monopolies e.g. one firm is able to satisfy the entire market at lower costs than two firms. Remember the Mediacorp and SPH forays into each other’s market? Small and local players are unlikely to take on Singapore Zoo or ST Technology anytime, given the characteristics of their industries which require high capital outlay.

Singaporeans should be more rightly concerned at the government’s tendency to pick winners. The government’s current role in the economy is most prominent in their attempts to nurture dynamic comparative advantage in promising industries. Other countries do so through protectionism or creating state-owned enterprises to monopolise the industry, but Singapore does it through fiscal incentives and infrastructure investments to attract FDI. Electronics, pharmaceuticals, tourism, digital media etc – these industries are not grown from the bottom, but deliberately nurtured from the top.

The problem with this is not the government’s inability to pick winners – pharmaceutical output was partly responsible for vigorous growth before last year – but economic development in Singapore has reached a stage where orderly planning may not lead to the next frontier. Technological innovations and capital stock accumulation are required to expand the economy’s productive capacity; attracting FDI has done a fine job, but the next step must be taken. Singapore needs to unleash the local, so-called ‘creative forces’ for long-term growth.

Temasek is a prime example of the government’s belief of orderly mobilisation of resources to tap on market forces. Temasek’s grip on some local giants such as Mediacorp and Singapore Power may be essential for national security reasons, but ownership and control of the vital companies by foreign firms can be limited through regulations. But from a commercial perspective, Temasek owns shares in them simply because they are profitable. Not everyone believes so, again, due to their image problem of being government-directed.

Temasek and the local giants symbolise the sometimes unfathomable economic thinking of the government. On one hand, it says it does not interfere in the commercial running of national champions; on the other hand, its continued stakes in them evokes a nagging feeling the government believes such firms should still be tied to their aprons, for unknown reasons. The Singapore government combines a strange mixture of socialist and free-market thought in the economy –national champions, state-led planning, heavy public subsidies on housing, healthcare and education; free-trader, fiscally conservative and aversion to welfare as to polyesters.

To be sure, Singapore’s development can be identified as ‘dirigisme and free markets’. But it is time the state reduces its direct influence. Signs have been encouraging; the government decided on two casinos, and both are now being built by foreign firms, not TLCs or GLCs. The ‘creative forces’ can come from both local and foreign, but it’s unlikely they will come from the government.

Likewise, the public should not waste its energy on the short-term losses of Temasek, but see the greater picture: Temasek as a symptom of the government’s forceful belief only it can secure Singapore’s economic future. It is time for the government to share the steering wheel with the private sector, and take a backseat, instead of driving the economy into their chosen road.

——–