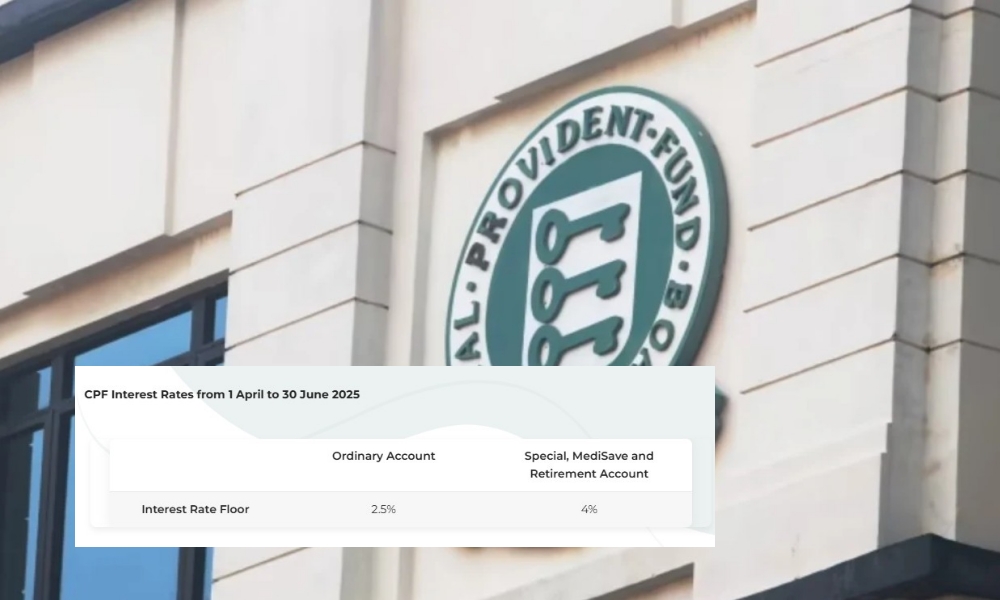

CPF Special, MediSave, and Retirement accounts' interest rate rises to 4.14% for Q4 2024

The Central Provident Fund (CPF) Board and Housing and Development Board (HDB) announced that the interest rate for CPF Special, MediSave, and Retirement accounts will increase to 4.14% in Q4 2024, up from 4.08%. The 4% floor rate will be extended for another year, providing members with stability amid a volatile interest environment, the announcement stated.

SINGAPORE: In a joint announcement on Friday (20 September), the Central Provident Fund (CPF) Board and the Housing and Development Board (HDB) revealed that the interest rate for CPF Special, MediSave, and Retirement accounts will rise to 4.14% for the fourth quarter of 2024, up from 4.08% in the previous quarter.

This increase, effective from October to December, comes as the pegged rate exceeds the established floor rate of 4%.