Current Affairs

Overseas Singaporeans risk being outlawed with Medishield Life?

By Howard Lee

By Howard Lee

Juliet Low has been working in the US and the UK for more than a decade, and never had to worry about high cost of treatment for her chronic illnesses. As a Singaporean working overseas, she is currently subscribed to the UK’s mandatory National Insurance, which covers the cost of her treatments in full. When she travels to Singapore for visits, she covers herself with travel insurance.

She has never relied on her Medisave in her working life. Not having worked much in Singapore, she does not have much in her Central Provident Fund account, which is currently used to make transfers into Medisave.

But that is set to change when the Medishield Life scheme comes into effect in November 2015, to supposedly provide universal healthcare coverage for all Singaporeans.

Under the Medishield Life Scheme Act passed in January 2015, all Singaporeans are required to pay premiums for the scheme and anyone who has not paid his/her premiums and who attempts to leave Singapore – which is very likely the case for Juliet – could be subject to severe penalties as a payment defaulter.

“A defaulter who, knowing that a direction has been issued under this section to prevent the defaulter’s departure from Singapore, voluntarily leaves or attempts to leave Singapore without paying the outstanding premium or furnishing security to the recovery body’s satisfaction for that payment —

(a) shall be guilty of an offence and shall be liable on conviction to a fine not exceeding $5,000 or to imprisonment for a term not exceeding 12 months or to both; and

(b) may be arrested, without warrant, by any police officer or immigration officer.”

The Act also grants authority to the police and the immigration office to “take such measures as may be necessary to prevent the defaulter from leaving Singapore until every outstanding premium has been paid or secured.”

These measure include “the use of such force as may be necessary” and “if appropriate, the detention of any passport, certificate of identity or travel document and any exit permit or other document authorising the defaulter to leave Singapore.” The government also retains the right to sue for recovery of outstanding premiums, although it is not stated in the Act if they can do so against Singaporeans residing overseas.

The Act could potentially affect Singaporeans residing overseas, which currently numbers more than 200,000 according to statistics from the National Population and Talent Division, and is growing by the thousands each year.

A group of Singaporeans living overseas, including Juliet and her friends, are now up in arms over the government’s threat to impose fines and imprisonment on those who fail to pay premiums. This is especially because Singaporeans who reside overseas are unlikely to benefit from Medishield Life.

But for Juliet and other overseas Singaporeans, the issue is not about being “recalcitrant” or not – she is more than happy that the scheme covers her parents, as it benefits them directly – but the idea of paying into a scheme that she does not use, does not even help with her real life medical expenses, and does not even resemble anything close to a healthcare plan.

“I don’t think the implementation is done by people who actually understand insurance,” she said. “I don’t think they are able to tell the difference in actuarial methods between life and health insurance.”

“Health insurance is like car insurance, which covers you on a year by year basis, unlike life insurance where you pay cumulative premiums over your lifetime in order to ensure coverage. If you don’t have a car, would you be expected to pay for insurance because you will get one at a future date? We should only pay for the relevant period of health insurance we wish to be insured.”

Indeed, the FAQ for the scheme suggests that the system has no provision as a life insurance plan, with no amount that can be returned to the payee or his/her family members.

“What everyone in the same age group pays ahead in premiums are pooled to help cushion the future increases in premiums during older ages. While some members may pass on earlier, the remaining pool of funds will need to help those of the same age who live longer and need to draw on more rebates.”

Many Singaporeans overseas already pay for mandatory insurance in their country of residence and for them, Medishield Life will unfairly increase their financial burden, especially since they would have no reason to use it.

The scheme has irked Juliet sufficiently for her to write in to the Ministry of Health to ask for clarification, but the answer has not been very different from what we have read in the news so far.

“We wish to share that MediShield Life was introduced to provide assurance to all Singapore Residents against large hospital bills for life, regardless of any changes in their health or life circumstances,” came the reply from MOH. “This enables all Singapore Residents to share in the national risk pool and play our part in supporting our healthcare costs.”

Singaporeans have been encouraged to write in to have their situation considered on a “case-by-case basis” but it is becoming apparent that many overseas Singaporeans who have contacted MOH or CPF have received the same email template with irrelevant references to the scheme, and have not had their situations considered at all.

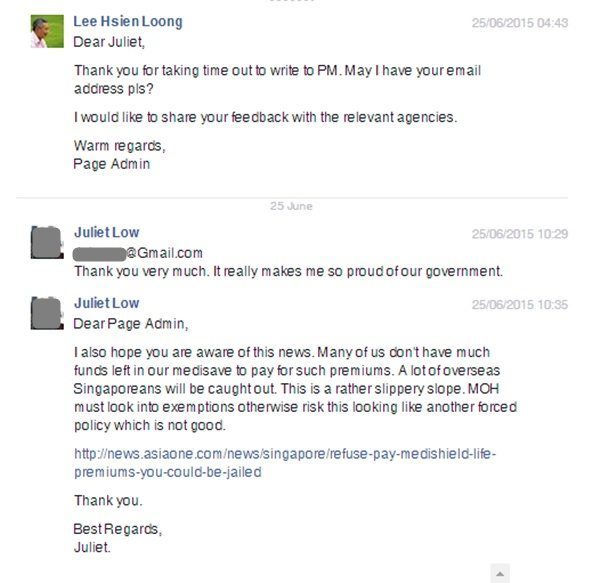

Juliet has since reached out to the Singapore embassy in the UK, and has been informed that they have contacted MOH on her behalf. The embassy has not received a reply from MOH as of 9 August 2015.

She has even engaged Prime Minster Lee Hsien Loong on Facebook, with a response by the page administrator to assist. But again, nothing thereafter.

For her, Singaporeans based overseas are facing a very real slippery slope as many do not actively contribute to their CPF accounts and hence do not enjoy the automated deductions towards Medishield Life premiums – they have no need to think about health coverage at home, as most host countries have strict requirements for them to purchase such coverage in order to work there.

But they now face a very real situation of being detained against their will should they return for a visit, or have government letters repeatedly served to their family members demanding them to help pay for premiums that will never be used.

Frustrated, she and a few others decided to start a petition to increase awareness about the situation that awaits overseas Singaporeans and to lobby the government to grant temporary exemptions for those already covered in their host country, and hence are in no way a liability to Medishield Life.

“The petition is not to challenge the government in implementing this as it is useful for those residing in Singapore, but it just doesn’t make sense for us (who are working overseas),” said Justina Lee, another Singaporean working overseas who is also raising awareness for the petition.

“We are not asking for full exemption,” said Juliet. “We are asking for an opt-out, (even to pay) a small admin fee, if we are sufficiently able to prove we will not need to use Singapore healthcare because we are covered. I do not believe this is unreasonable. If we decide to return to Singapore, we will then opt-in again and pay premiums for the relevant period.”

As the November 2015 deadline draws near, any promise by the authorities to consider the situation of overseas Singaporeans on a case-by-case basis have appeared to be ineffective, and many overseas Singaporeans have begun to feel that healthcare coverage could be the tipping point for many Singaporeans who have been out of the country for decades.

“I fear that the brain drain will become permanent as many have spoken about relinquishing their citizenship altogether,” said Juliet.

“I love my country and I want to remain a Singaporean for the rest of my life, but I simply can’t afford to pay for medical insurance in two different countries,” said Justina. “If this goes ahead, I fear I will be forced to give up my citizenship which is also my roots and identity.”

Juliet also questioned the logic of scheme trying to cover Singaporeans working overseas. “Why would overseas Singaporeans, who are fully covered in their local jurisdiction, rationally return to Singapore to use the healthcare there? Why force us to pay for something that we would never use? Who is in the committee that they say are actually considering our appeals on a case-by-case basis?”

She and other overseas Singaporeans are also eager to open the doors of consultation between overseas Singaporeans and the CPF Board, MOH and the Medishield Life Council in order to reach an amicable solution.

“We are educated and well-travelled,” said Juliet. “We have experienced medical systems from around the world. We can help provide guidance for a better implementation of this scheme. Let us help. But first, hear our voice. Do you really wish to imprison us all?”

To support Juliet’s petition and share her concerns, you can sign the petition online.

TOC has approached the Ministry of Health for clarification on this matter. At time of publishing, we have yet to receive a reply, but have received a commitment that they will respond. We will include their response once received.