Community

Only persons with severe disabilities allowed to receive $600 monthly from Careshield, Facebook user claims

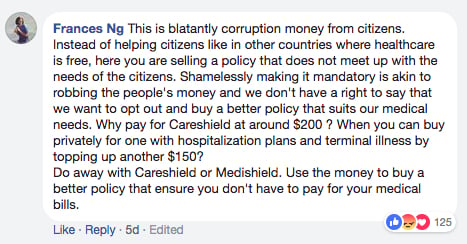

A Facebook user by the name of Frances Ng has made a claim that only persons with severe disabilities are entitled to receiving a monthly payout of $600 from Careshield.

In her post dated 30 June, Ng noted that the premium paid over the years is non-refundable “if you are not severely disabled”.

Consequently, she alleged that the savings of persons who had placed their money in the CPF is in fact used in the process of “amassing the country[‘s] sovereign funds for GIC [Pte Ltd] and Temasek Holdings to invest”.

She ended her post by expressing her concern over the matter, suggesting that Careshield’s coverage is far from adequate in covering medical expenses in Singapore.

She extended her commentary on the matter in a comment below her post:

Screenshot of Frances Ng’s extended commentary, on the issue of Careshield’s payouts being limited to persons with severe disabilities.

She added in a separate comment: “A lot of people think that Medishield is government money but they didn’t know it is part of your CPF money. It is your hard earned money.”

Yeo Boon Teck confirmed Ng’s sentiments:

My father suffered a heart attack in 2015. While staying in the ICU ward, doctor scheduled to do ballooning by next morning. That morning, I was away to attend a work meeting. NUH called me to rush down to attend a counselling session to understand and agree upon the costs first before they can proceed. They cannot proceed without me attending the session, even [when] I told them [that] we are all Singaporean[s] and my dad has CPF. Also cannot. Must talk money first.

Francis Ong is appalled by the issue stated in Ng’s post:

Where is KBW [Khaw Boon Wan]? Didn’t he tell people he paid $8 for a heart bypass? Is he lying? Did he get special treatment because he is a minister? Did he misuse his authority to get unfair advantage? We need an answer for this definitely!

William Hidajat also responded to the post, stating:

It is also important for citizen[s] to know since MediShield [was] implemented in 2015, how much [money] was collected? The insurance companies should also publish the number of citizens giving up their private insurance policies since MediShield [was] implemented.

[…]

The ministers in this country earn salaries [that are] quite high and they [do] not need to subscribe to the MediShield, [thus] they still can afford fees[,] but for the citizens, they need to go up north to buy medicines.

Adrian Pah wrote:

Medishield Life only covers Class C wards. And there is also an excess payment of 10% of total bill and co-payment of $1000 to $4500… There is also a Maximum claimable for every service provided, i.e. ICU… Operation. Daily limits… et cetera. But why for life, when even his father didn’t live past age 92? Before this, LifeShield already covers up to age 92… Why pay 30% to 40% more premium to cover that age, when 98% of Singaporeans will be dead [by then]… Isn’t that a scam..??? Sucking 30 to 40% of our CPF funds.

Francis Chuang was baffled by the CareShield policy:

Forcing a 30yo to [be] group[ed] under [the] senior [citizen] category is ridiculous.

Jim Lion posted a seemingly neutral take on the matter:

Careshield is just another insurance for disability except that it is compulsory. Like all insurances you don’t get back your premium if the covered event don’t happen to you. From a policy pov they are making it compulsory for everyone to have the biggest pool, spread the risk among the whole population n keep the premium the lowest possible. That’s the theory. Whether Sinkies is getting a good deal would depend on comparing it with other similar disability insurances from others, you have to compare an apple with other apples.

User 陈 秋燕 (Qiu Yung), however, has accused Ng of fabricating her account of the issue:

Obviously a story that is made up in order to make people unhappy. The fact is that subsidy for a C Class ward starts at 65% of the bill.

Come up with a more convincing story next time. Better still, stick to truth. Why fabricate?

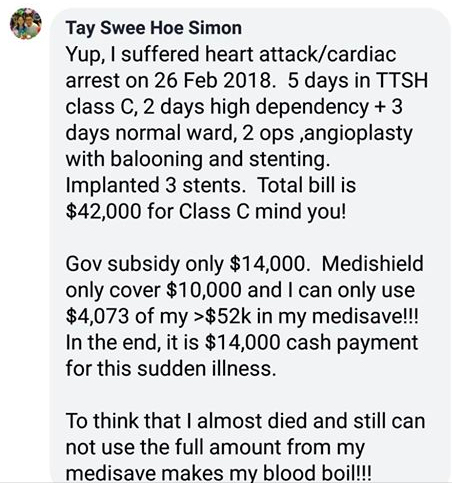

However, Tay Swee Hoe Simon rebutted Qiu Yung’s comment in support of Ng’s claim:

“My story, I have the bill and receipt to prove it. Plus, I am alive to tell the story! 65% subsidy for class C patients is bull shit”

Nazari Isa made a retort against Ng’s post:

Classic case study for fake news. Read an article, then read other sources to verify facts. Is the Facebook profile genuine? Does the Facebook profile have an ulterior agenda? Do other sources match? Bottom line, don’t jump to conclusion[s]. Check first.

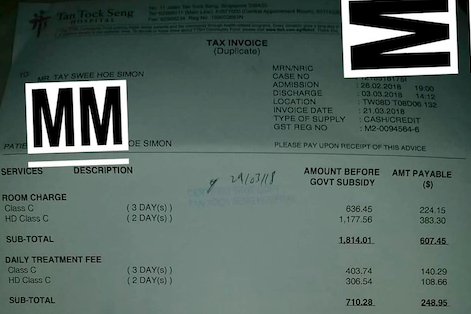

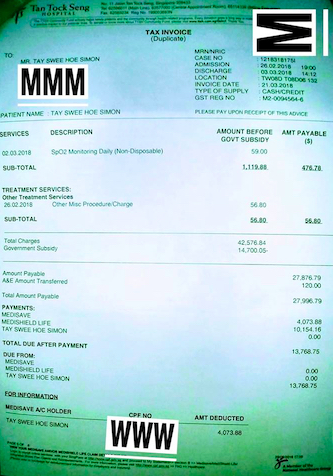

Tay then responded with photographs of a couple of pages from his hospital bill in new comments, suggesting that no false allegations were made regarding CareShield and MediShield:

In one of her subsequent comments, Ng recommended the following to Facebook users who have commented on her post:

“Premiums paid are not refunded. Better stay put with ElderShield.

Buy a private hospitalization and terminal illness plans and with rider, if there is enough Medishield to pay for the private policy.”

On 4 July, it was reported that CPF members can only withdraw money from their own CPF if they are at least 30 years old and “severely disabled”.

Persons with severe disabilities will be allowed to withdraw cash from their Medisave account in CPF. However, they or their spouses must have at least $5,000 in their Medisave accounts in order to be able to withdraw $50 on a monthly basis.

Those with $20,000 or more in their Medisave accounts will be allowed to withdraw $200 a month, according to The Straits Times.

The sum covers about half the people aged 65 or older, who are more likely to suffer from severe disabilities.

This is the first time that CPF members will be allowed to withdraw cash from Medisave since the CPF’s establishment in 1984.

Starting 2020, persons with disabilities will receive $600 per month for life under a long-term disability insurance called CareShield Life, according to The Straits Times.

CareShield Life will be made compulsory for people aged 40 years and younger.

A new contingency plan called ElderFund will provide people with disabilities who are in need with up to $250 a month, beginning in the same year.