Commentaries

No matter how high prices are, HDB flat as an asset will depreciate given the reversion to zero

by Chris Kuan

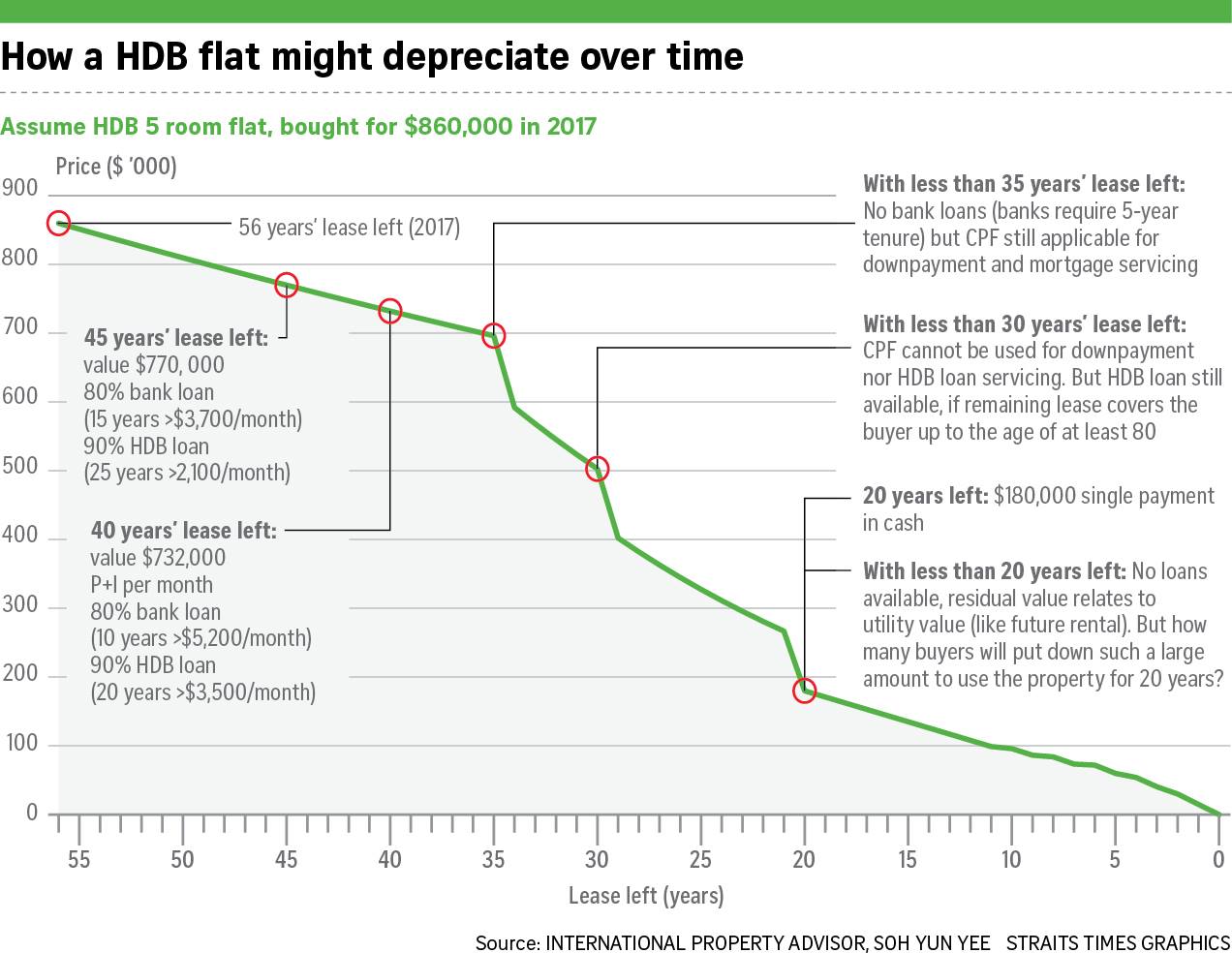

Look at this chart from International Property Advisors reproduced by the Straits Times and you’ll be thinking “Asset enhancement? What asset enhancement?”.

Hence the tune has changed to “good store of value” but even so, you should be thinking “Good store of value? What goodstore of value?” – is it a good store of value when the asset gets depreciated over time?

“My last blog on choosing a HDB resale flat generated some discussion and debate. Let me share some additional perspectives.

HDB flats, like many private properties, are sold on a 99-year lease. They provide a good store of asset value, so long as you plan ahead, and make prudent housing decisions.

To begin with, Singaporean couples enjoy significant subsidies when they purchase a HDB flat for the first time, be it a new flat or one from the resale market.

Take for instance a 30-year-old couple, with a combined monthly income of $5,000, looking for a resale flat in Woodlands near their parents.

They can get up to $75,000 in grants off the resale flat price, and should easily afford a flat with a reasonably long lease of 90 years.

35 years later, the couple will be 65 and the remaining lease of the flat will be 55 years.

They still have an asset which can be monetised for retirement.

In fact, this is already happening in Woodlands.

A 65-year-old elderly couple living in a 4-room flat with 55 years of lease remaining in Woodlands can sell their flat and right-size to a nearby 2-room Flexi flat with a 30-year lease.

They can enjoy a Silver Housing Bonus of $20,000 in cash. They can also get quite a lot of money from the sale proceeds – around $100,000 upfront in cash, plus $500 per month of additional income for their retirement (on top of what they would get through CPF Life).

Alternatively, if they prefer to stay in the same flat, they can apply for the Lease Buyback Scheme or LBS. This means they continue living in the flat for 30 years and sell the remaining 25 years back to HDB. They can enjoy a cash bonus of $10,000. In addition, they will get $47,000 in cash plus $400 a month for retirement (again on top of CPF Life).

The cash amount is not as much as if they were to right-size, but that’s because they can continue to stay in the same flat, and also have the option to rent out a room.

I have given some simple examples. But they are typical of many HDB households.

The general point is that your HDB leasehold flat is not only a good home, but also a nest-egg for future retirement needs.

That’s what we have achieved and that’s what we will continue to ensure – both now and in the future.”

Mr Wong’s explanation is both valid and reasonable strictly within the context of government objective of letting leases revert to zero.

But the point is this works only if there is a appreciation in HDB values in the initial years of ownership. Subsequently, no matter how high prices are, HDB flat as an asset will depreciate given the reversion to zero. If prices don’t go up, then it is really unlocking residual value from a depreciated asset. This is unlike many countries where the lease can be renewed at 3-5% of assessed rated value, hence an implied asset value to the leaseholder should the property be taken back by the freeholder (in our case the government).

Now to the point of today’s post. The establishment has made it a habit of implying that Singapore’s approach to retirement and healthcare funding, i.e. using HDB flats as “store of value” to be monetized, as somehow superior to the European nations by repeatedly disparaging their pay as you go approach as risky and burdening future generations. What is conveniently left unsaid, is that when the older generation monetized their HDB flat, the money does not appear out of the thin air.

Then who contributed the monies the government paid to the older generation other than the younger generation who paid up for their new HDB flats? Isn’t this rather the same as the pay as you go European system except instead of going through the tax and spend system, we in Singapore go through the medium of real estate prices?

And isn’t this even more risky given that the edifice is dependent on maintaining real estate values through immigration and foreign worker influx? This is kicking the can into the future because at some point the population will stop growing.

The bottomline is that there is no magic bullet to solve pensions and healthcare funding. There is really no alternative than through tax and spend policies.

The surprise is we continue to believe there is.

This post was first published at Chris Kuan’s Facebook page and edited with permission.