Finance

Markets endorse Trump’s victory

By Margaret Yang, CMC Markets

A surprise risk-on rally

Global risk assets unexpectedly rebounded on Donald Trump’s victory in the US presidential election last week, along with a fast sell off in safe-haven assets including gold and the Japanese yen. This “post-election” rally mirrored what happened in the “post-Brexit” rally and it once again proved that bad news can be read as good news to the stock market. The risk-on sentiment was fueled by ample liquidity and ‘certainty’ brought by the election results. No more surprises before Christmas, please.

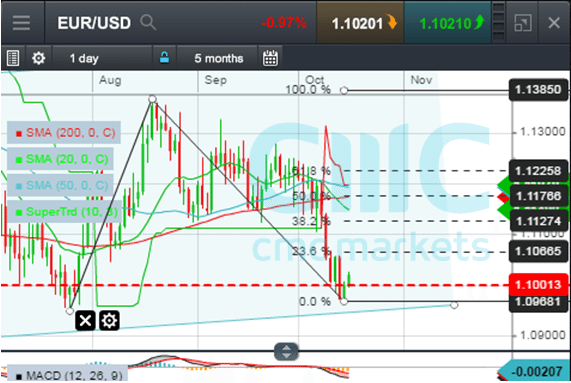

Federal Reserve Vice Chairman Fischer said on Friday that “The case for removing accommodation gradually is quite strong”, hinting that a December rate hike is on the table. The Fed was reasonably close to meeting its inflation target and full employment, which justifies a 25 bps rate hike by the end of this year. A high expectation – over 80% probability of a rate hike – has been priced into the futures market. And dollar index has surged to its highest level this year to nearly 99.50.

Commodities collapse as US dollar index heads towards 100

A strong dollar weighs on commodities, especially precious metals and crude oil. For WTI Dec contract, immediate support levels are $43.80 and $42.00 respectively. Gold prices have broken key support level at $1,240 and the next support level is around $1,195 area.

US S&P 500 index surged 4% last week and is now testing key resistance level around 2,178 points. The upward momentum will probably slow down near this level as the market is facing the increasing likelihood of a rate hike, and ‘risk premium’ associated with Trump’s presidency will eventually have to be priced into the stock market.

US Dollar Index Dec 2016

Margaret Yang Yan, CFA, is a market analyst for CMC Markets Singapore