Unwrapping the global financial crisis

A global problem requires a global solution. By <b>Donaldson Tan</b>.

Donaldson Tan / Writer

Although the immediate outlook for the world economy looks grim, the historical experience of the emerging markets pulling the world economy along will point the way forward when recovery gets under way. As the global financial crisis continues to unveil itself, leading OECD economies were already on a united dive into recession, driven by simultaneous collapse in consumer and business spending and the rising threat of job losses and bankruptcies. A vicious cycle emerges: deteriorating economies drag down prospects for companies and debt defaults, which further damages the financial markets and thus the economies concerned.

As the global financial crisis continues to unveil itself, leading OECD economies were already on a united dive into recession, driven by simultaneous collapse in consumer and business spending and the rising threat of job losses and bankruptcies. A vicious cycle emerges: deteriorating economies drag down prospects for companies and debt defaults, which further damages the financial markets and thus the economies concerned.

For the financial economy, the problem is greater than simply adding up the bad debts. The mark-down of all debts (good and bad) on the basis of the dramatic slide in asset prices has an insidious effect. Such a mark-down has the potential to destroy more financial institutions. Few have the cash and reserves to readily cover the gap, and raising new funds in current conditions is virtually impossible.

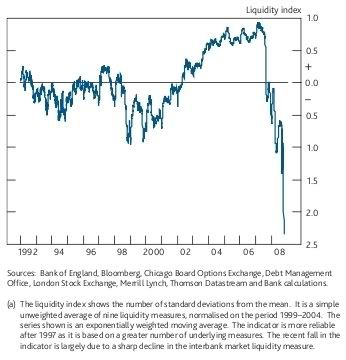

(Left: Figure 1: Financial Market Liquidity)

This is best demonstrated by the rapid disappearance of the bulge bracket US investment banks.

1. March 2008: Bear Stearns was taken over by JP Morgan.

2. September 2008: Bank of America purchased Merrill Lynch.

3. September 2008: Lehman Brothers filed for bankruptcy.

4. October 2008: Goldman Sachs & Morgan Stanley become commercial banks.

For household and companies alike, the risk is no longer limited to cutting down on budget. The immediate threat is the freezing up of credit and the struggle to access working capital that pays wages and input costs. The loss in spending already in the pipeline is enough to cause a nasty global recession: GDP will probably fall by at least 1-2% in the US and Europe in 2009. However, taking into account the current turmoil, the drop in US and Europe GDP could escalate to proportions more typically seen in Third World debt crises. Some pessimists have estimated a drop of as much as 10%.

To illustrate the stark impact of the credit crunch, the State of California is having problems with credit lines necessary to pay teachers' wages. During the 1997-98 Asian Financial Crisis, Asian companies could not even get the finance to ship goods out of the factories and the ports. It is no wonder that the ASEAN labour ministers recently warned that job cuts would be expected in the region.

Will recession engulf the global economy?

In general, economic decoupling refers to the growth in one area of the world economy becoming less dependent on growth in another area. Up to mid-2008, the emerging market economies remained strong and the process of decoupling from US and European economies that had been in evidence for some years offered the hope that they could keep world growth going. However, the global financial crisis has deepened so dramatically that the validity of the decoupling theory is starting to show cracks.

Although the emerging market economies‘ growth rates are much higher than the OECD average rate, and this gap has widened, the cyclical pattern for most years is very similar. In other words, OECD and the developing world growth rates continue to be highly correlated. Decoupling is only a temporary phenomena. Sustained high growth in the emerging market economies has been supported by successful diversification in the engines of growth, with stronger dynamics in domestic consumption in the emerging market economies offsetting slower growth exports to OECD countries.

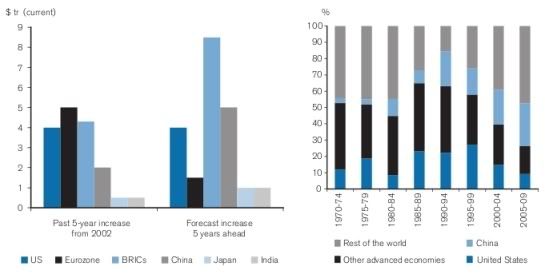

(Right: Figure 2: Contribution to Global GDP (Source: IMF)

In fact, the share of emerging market economies‘ exports to the US has dropped below 15% of the total from the peak of about 25% in 1997. Diversification reduces exposure to specific risks but it does not rule out systematic risks. It is widely thought that the global financial crisis is the result of over-flourishing of systematic risk in the global financial system. This view was in fact echoed in Couterparty Risk Management Policy Group‘s submission Containing Systematic Risk: The Road to Reform to the US Treasury Secretary Henry Paulson in August 2008. A systematic overhaul of the global financial system is overdue, but there is no quick-fix solution that can halt a global recession.

Will China rescue the global economy?

It is widely regarded that the Chinese economy will play an important role in limiting the damage of a global recession. After all, China has been the mainstay of world growth over the last couple of years. The growth dynamics of the Chinese economy has shifted markedly in favour of domestic demand over the export-orientated model. While the IMF forecasted Chinese economic growth for 2009 to be 9.3%, Standard Chartered Bank forecasted 7.3% for the same period. It is expected that Chinese demand will continue to act as drivers for growth globally and regionally.

A consumer boom has finally materialised after many years of the Chinese government trying to boost spending and curb excess savings. Such policies include taxing savings accounts and granting more public holidays. Chinese retail sales in 2008 have grown by more than 20% while investment growth remained high at 25%. At the same time, soaring Chinese exports to the rest of Asia and other high-growth regions have taken over sales to the US as the main drivers of export growth.

The Chinese government, which has currency reserves of US$1.9 trillion, has announced a series of measures to address the bleak economic outlook. The Chinese government will increase infrastructure spending, raise export tax rebates, reduce property transaction fees, encourage banks to lend more money to small- and medium-sized companies, and introduce new programmes to support farmers. Furthermore, economists expect the central bank to cut interest rates for the third time this year.

Last but not least, inflation is not a threat. There are severe excess capacities in many Chinese business sectors, so businesses would have to lower prices in the domestic market at a time when China‘s exports to the US, which accounts for 21-23 per cent of China‘s goods and services, are slowing down. The RMB, which has been rising in tandem with the US$, is counter-intuitively boosted by the credit crisis. This is due to fears that the financial crisis in Europe is even worse than in the US. The strengthening of the RMB against most currencies is therefore deflationary for China.

However, there are warning signs in the Chinese economy that cannot be taken lightly. The Chinese government‘s main price index for 70 cities fell modestly last month. There is also more conclusive evidence of an impending slump in the market. Last year, the number of properties sold increased by 26%, but in the first half of this year, it fell by 11%. In August 2008, the amount of floor space under construction fell. This was backed by weak figures for steel and cement production. Car sales grew by 23% last year but it fell by 5% for the first half of this year. On the other hand, real urban income only grew by 5% for the first half of this year, whereas it grew by 12% last year.

The light at the end of the tunnel

Persistently high global growth has been due not just to the sustained buoyancy of emerging markets, but also to the greater impact this now has on global GDP because of the rising weight of the emerging markets in the global GDP. A non-OECD recession must involve additional risks such as a slump in the domestic investment and consumer confidence.

Although the immediate outlook for the world economy looks grim, the historical experience of the emerging markets pulling the world economy along will point the way forwad when recovery gets under way. Growing cooperation across central banks in the face of a serious and common challenge is also a positive development in mitigating the risk of a global recession. The degree to which all countries have seen similar impacts and responses to the crisis has heightened the sense of all being in this together.

Perhaps this bodes well for further global policy coordination in other arenas. After all, a global problem requires a global solution.

----------