Finance

Singapore’s $2.8b money laundering scandal casts shadow over Shanmugam’s regulatory claims

In late March this year, Minister Shanmugam dismissed comparisons likening Singapore to the Cayman Islands, citing rising capital inflows. He asserted Singapore’s status as a ‘serious’ financial center with robust regulatory frameworks.

However, revelations from the S$2.8 billion laundering case depicted illicit monies flowing into the city-state, with the ten accused extravagantly spending their wealth and establishing family offices seeking a ‘safe haven’ in Singapore.

The crackdown on a high-profile S$2.8 billion money laundering case in Singapore on 15 August sent shockwaves not only through the city-state but also reverberated across international headlines.

Singapore has long been focused on attracting the ultra-wealthy, resulting in a thriving finance industry that has positioned the country among the world’s wealthiest.

However, this recent case has triggered a significant reassessment of these practices amid concerns that illicit funds may be infiltrating legitimate businesses in Singapore.

Worries over potential risks arising from Singapore’s ease of access and convenience for foreign wealthy individuals have been raised long before the 15 August crackdown.

International news outlets such as Bloomberg and the Financial Times (FT) have highlighted the intriguing phenomenon of an influx of ultra-wealthy families from China into Singapore.

Concern over Singapore’s competition with global offshore centres

In a notable March article, FT published a headline-grabbing piece titled “Singapore and Hong Kong Compete to Become the Prominent Financial Centers of Asia,” highlighting the rivalry between the two cities to become the leading financial hubs in Asia, aiming to shift the global centre of gravity for hedge funds and wealthy families.

The article emphasized the establishment of innovative fund structures – Singapore’s “variable capital company” (VCC) and Hong Kong’s “open-ended fund company” (OFC) – directly challenging traditional offshore financial centres such as the Cayman Islands and the British Virgin Islands.

According to government data, there were 872 registered VCCs in the city-state as of February. This surge contributed to a record S$448 billion in total asset management inflows during 2021, marking a 15.7% increase from the previous year, according to the most recent data from the Monetary Authority of Singapore, the island nation’s central bank, and financial regulator.

Moreover, Singapore’s VCCs have benefited from the rapid expansion of another segment within its asset management industry: family offices. Significant amounts of family wealth shifted to the city-state during the pandemic, especially from mainland China, surpassing even the growth seen in VCCs.

However, the FT article also sounded alarms about potential risks associated with these structures, such as money laundering and tax evasion, stemming from the opacity and privacy they afford.

K Shanmugam dismissed the comparison to Cayman Island, emphasizing Singapore’s robust regulatory frameworks

Following this, the Singapore Minister for Home Affairs and Minister for Law K Shanmugam, during an interview with the South China Morning Post (SCMP) on 29 March, dismissed comparisons drawing parallels between Singapore and Hong Kong with the Cayman Islands due to increased capital inflow.

Shanmugam unequivocally affirmed the serious nature of both Singapore and Hong Kong as “serious” financial centres with robust regulatory frameworks.

“When I want to transfer $5000 from one account to another, the bank asks me questions. My own money. That’s Singapore, ” he said this exemplifies the calibre of Singapore—an environment where clean money prevails, leaving behind the era of dubious dealings.

“Hong Kong and Singapore, both, are centres which are world-class, with good regulatory framework, and there is enough clean, good money that you can deal with. ”

Shanmugam hinted that such comparisons might be driven by envy from less attractive financial centres that are losing their appeal.

“Because perhaps the centres which are losing out, which could be attracting this money, are not as attractive as they once were, and many of these newspapers are stationed in those countries.”

“Today, look at financial centres, isn’t it obvious that there are some places in the world which have long harboured – and we are talking about top financial centres in the world – which have long harboured questionable money? And I’m not referring to Singapore and Hong Kong. ”

“So, I think when you live in glass houses, you have to be careful about throwing stones, ” he told SCMP.

Responding to the SCMP reporter’s inquiry regarding potential social divisions caused by the influx of wealth and talent, Minister Shanmugam acknowledged the issue and emphasized Singapore’s proactive steps to tackle it.

Despite Singapore’s provision of opportunities and fundamental needs for its citizens, disparities due to global competitiveness are inevitable, according to Shanmugam.

He underscored Singapore’s distinctiveness as a sovereign city-state without alternative regions for relocation, stressing its reliance on global competitiveness for economic growth due to the absence of abundant natural resources.

“In any such competition, there will be winners and there will be people who don’t do as well. The Government makes sure that most people’s basic needs are taken care of – as long as they work hard. So it doesn’t matter if you don’t reach the top – you will still have a decent life. ”

The Minister acknowledged that being a global city attracts talent and resources but stressed the importance of ensuring equal opportunities for those with the ability and supporting those who may not reach the highest echelons of success.

At least five family offices in Singapore linked to 10 accused in S$2.8B money laundering case

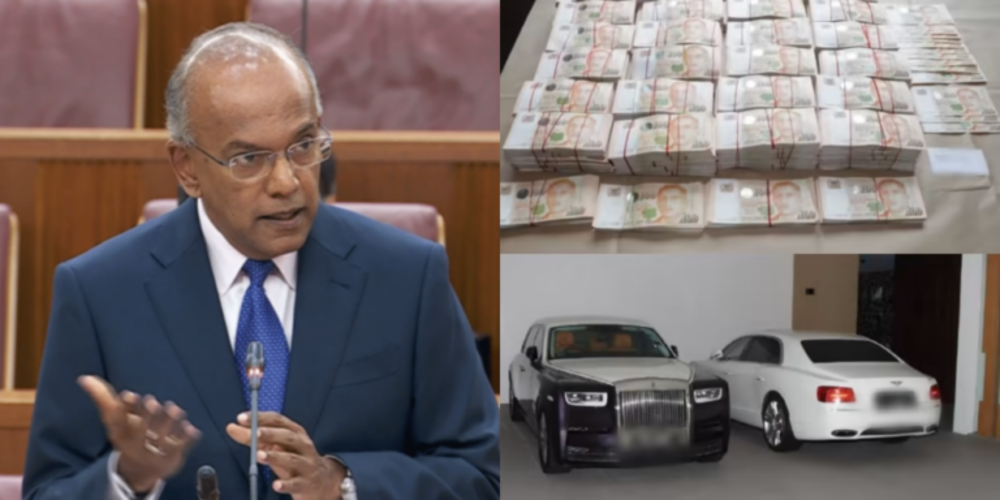

Despite the Minister’s emphasis on Singapore’s robust regulatory frameworks, the ongoing investigation into the city-state’s high-profile S$2.8 billion money laundering case has unveiled shocking revelations for Singaporeans.

On 15 August, ten suspects were arrested in an islandwide anti-money laundering probe mounted by the police in an operation that has been described by the prosecution as unprecedented in size and scope.

The seized assets encompass a wide range, including 152 properties and 62 vehicles with a collective estimated worth exceeding S$1.24 billion.

Additionally, the authorities have confiscated more than S$1.45 billion in bank accounts, over S$76 million in cash, and cryptocurrencies valued at more than S$38 million.

A recent in-depth report from Bloomberg unveiled that among the 10 accused individuals, there are at least five family offices linked to them.

In a parliamentary session on 3 October, Minister of State for Trade and Industry, Alvin Tan, revealed potential links between one or more of the accused in the significant S$2.8 billion money laundering case and the establishment of an office that received tax incentives.

Tan clarified that Single Family Offices (SFOs) seeking tax incentives from the Monetary Authority of Singapore (MAS) must demonstrate proof of opening accounts with local financial institutions.

“At the point of application, no adverse information of note related to the individuals and entities had surfaced,” Mr Tan said.

Due to ongoing investigations, Tan refrained from disclosing whether these SFOs still receive tax incentives when queried by MPs. He stressed MAS’s commitment to enhancing checks and terminating incentives, where necessary.

However, MOS Tan defended the significance of family offices in Singapore’s financial landscape, cautioning against generalizing all SFOs based on the actions of a few implicated ones.

“We have just completed the consultation, which will enable us to tighten some of these processes, but we remain open as the other Ministers and I have mentioned – to talent, to investments as well as to financial flows, including those in SFOs. ”

“Our regime is in line with international best practices, and so, these two prongs of making sure that we are dynamic and open, and that we also have strong robust controls, remain central to our functioning as a vibrant and trusted financial centre,” he told the Parliament on 3 Oct.

The number of family offices in Singapore grew substantially, with more than 1,100 established worldwide by the end of 2022, marking nearly a threefold increase from 2020.

Many of the accused individuals not only invested in existing companies but also created their own ventures, thus establishing various connections within the country.

These developments have led Singaporeans to ponder significant questions, particularly regarding the ease with which these accused individuals managed to register a shell company in Singapore, seeking a perceived “safer haven” within the country’s boundaries.\

This article was first published on Gutzy Asia.