Editorial

Temporary piecemeal measures cannot control the escalating prices of public housing in Singapore

Just yesterday (29 Sep), the Singapore government announced measures introduced to promote sustainable conditions in the property market by ensuring prudent borrowing and moderating demand.

Of the measures announced, the Housing Development Board (HDB) will introduce an interest rate floor of 3% for computing the eligible loan amount from 30 Sept onwards and the loan-to-value (LTV) will be lowered by 5%-points from 85% to 80%. These apply for housing loans granted by HDB.

Not too long ago, HDB had already announced a reduction of limit for housing loans from HDB from 90% to 85% in Dec 2021.

This close sequence of control measures would indicate to some that something must have been so troubling for the government to have elicited such a reaction.

Truth be told, many members of the Singapore Parliament filed questions to the Ministry over the past year for updates on the affordability of public housing following resale prices of HDB flats rising for 26th straight month in August.

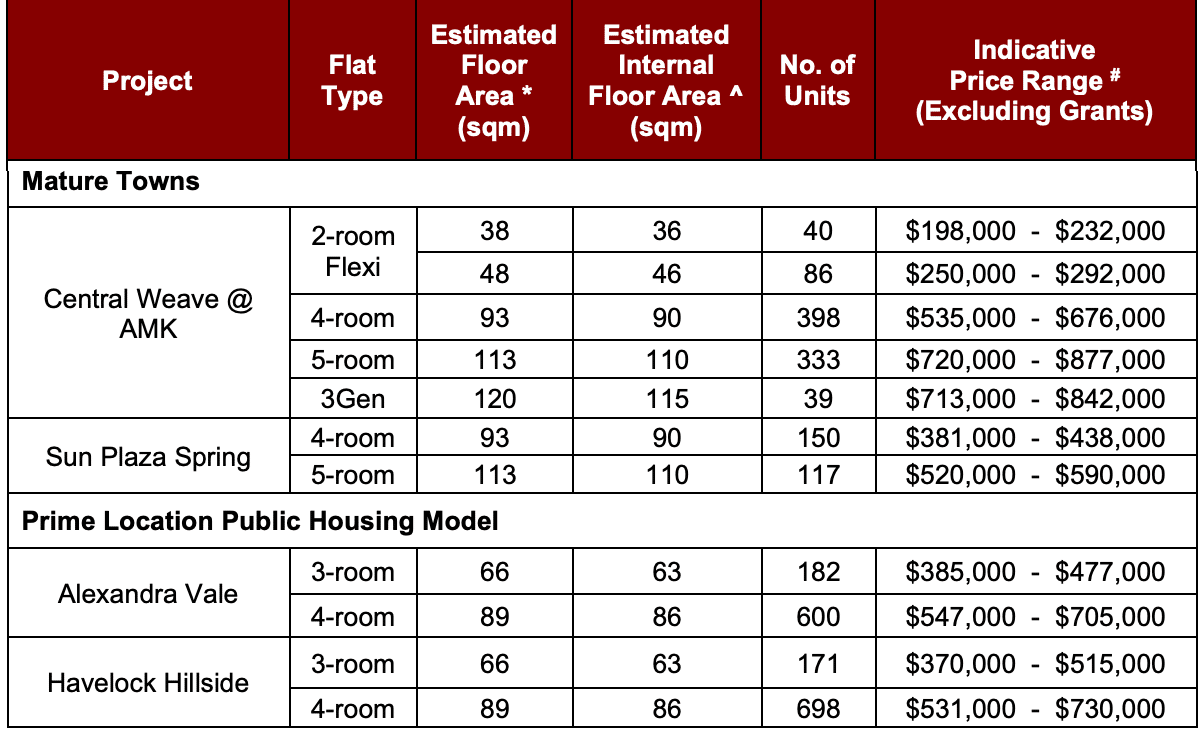

TODAY reported just last week that it is only “a matter of time” before Singapore sees its first million-dollar BTO flat, based on opinions voiced by property analysts.

Beyond mere speculation, one can easily see that horizon nearing us with the top end of a 5-room flat offered in the August BTO launch at Ang Mo Kio being priced at S$877,000. One can even say it is not impossible for resale flats to reach S$2 million in 20 years’ time.

Even with the introduction of a minimum occupation period (MOP) of 10 years before buyers can sell their flats in the open market or invest in a private residential property, it is still not far-fetched for people to continue the perception that the HDB balloting for new BTO flats — particularly those in mature estates — is a form of lottery where one can cash out their earnings after a period of time.

It is pretty obvious from MND’s own data which was made available in response to Workers’ Party MP, Mr Leon Perera that it would be a definite profit if one were able to sell the balloted flat after the MOP regardless of the 5 or 10-year MOP.

Take the median price for a 5-room flat bought in 2012 which is S$376,000 and supposed it is sold ten years later at the median price provided by the Ministry at S$530,000. That is a hefty profit of S$154,000. This would probably even be much higher for flats in mature estates such as Ang Mo Kio at the median price of $785,000 for a five-room flat in 2022.

Of course, the profit drops for units below 4-rooms but at the same time, this is the same reason why most couples with the means of buying a larger unit, would choose to do so.

So what if the BTO flats become $1 million? The buyer can just seek to sell it off at a higher price ten or twenty years down the road. There is, after all, no cap on how much a flat owner can sell the flat in the resale market so long as there are willing buyers.

Measures Do Not Control Rising Cost But To Make Those Who Cannot Afford Ineligible

Going back to the latest response by the Singapore government to introduce control measures, frankly, it does not seem to do much other than making the flats which had seemed costly for the citizens, to be totally out of reach from them.

Of course, the government will continue to say that HDB flats are affordable.

In his response to Mr Perera’s parliamentary question, Mr Desmond Lee, Minister for National Development wrote that flat owners only need to use 13% to 26% of their monthly income to pay for their loan instalments. This is well below the international benchmark of 30% to 35%.

But Mr Lee’s justification is kind of questionable given that flat purchasers would have to meet the qualifying criteria to apply for an HDB loan (such as income) in the first place.

For example, using the regulation set by HDB on housing loans, even if the price for a BTO HDB unit is S$1 million, Mr Lee’s answer to Mr Perera would still stand because the flat owners have to first qualify for the loan with their proof of income and ability to pay for the down payment before they could purchase the flat.

Unrestrained Hike In HDB Prices Unsustainable In The Long Run For The Past And Future Generations

It is in the interest of the government that the price of HDB flats continues to rise. After all, it is definitely the main culprit for the escalating price of public housing by tying the valuation of BTO flats to the prices of surrounding resale flats. On top of that, people are still being sold the idea that HDB flats can be cashed out at the end of the day for their retirement fund.

But if you noticed by now, this pricing method of property premising on the idea that you can “definitely” cash out with a profit, will eventually spiral out of control for the general masses. Especially since the average salary for ordinary citizens will not be able to keep up with such rate of inflation — Note the position taken by Deputy Prime Minister and Finance Minister where he cautioned against increasing wages too quickly and how it could hurt Singapore’s economy.

Let us also not forget that we are talking about affordable public housing for the common folks here and not private housing meant for asset appreciation or speculation.

With the Ang Mo Kio SERS saga that has yet to be resolved, we can see the pitfalls of the current public housing scheme for seniors. Where if you are forced to sell your flat when it is aged, you are greeted with the harsh reality that the cost of getting a new flat requires you to come up with a huge cash upfront when you are already retired.

In a way, this also dispels the common belief that you can comfortably retire with the proceed from selling your HDB flat as you would nevertheless require an alternative place to stay. While you might be able to afford one by downsizing and going for a shorter lease, it is questionable if you benefited from such a transaction, given the displacement and marginal profit if any.

Alternatives Moving Forward And Going Back To Our Roots

Various entities have proposed alternatives for Singapore’s public housing particularly since issues arising from high prices and aging HDB flats have gradually stroke concerns of the flat owners.

Read: Singapore public housing policy: Comparing amendment proposals from WP, SDP & FOSG

Personally, I would think that the ideal way forward would be delinking the BTO price from the surrounding resale flats and mandating that all future sales of flats be made with HDB only. At the same time, allowing existing flat owners to continue with the resale market. This will ensure prices for HDB flats do not depreciate rapidly, eating into the assets of the flat owners, at the same time, preventing the vicious cycle of escalating prices for HDB flats — especially for the sake of the future generations of Singaporeans.

But of course, this has to be done in phases over an extended period of time for the market to properly react to the changes, coupled with other control measures such as disallowing Permanent Residents from purchasing HDB flats and reduction or removal of the land cost from the cost of flats.

Ultimately, Singapore as a country has to decide what public housing means for the people.

Is it a policy for the government to profit out of the people’s desire for home ownership, the average citizens’ means of having an appreciating asset for one’s retirement or a public policy to ensure all citizens regardless of their background and family heritage, able to have a roof over their heads and live with dignity?

Let us look back to the roots of public housing in Singapore, a policy in the 1960s that allowed many who were living in slums to have access to cheap, clean and safe accommodations; A public policy that has been the pride of Singapore citizens and the cause of envy from our neighbouring countries and the international community.