Property

Case Study: A curious case of “no money down” property schemes

We present the case of John and his parents. John is an undergraduate student who has taken finance and investment classes that cover a range of asset-types, including real estate. During a family dinner, when discussing a module that John was taking in the university, Real Estate Investments and Finance, his parents divulged that they have made a real estate investment several years ago: a 3-bedroom freehold condominium unit in Johor, Malaysia.

Their decision to commit was based on 3 key factors:

1. They believe that real estate is a safe asset that will constantly grow in value. If held for long enough, the capital gains will return a hefty sum. Surely, real estate is a worthwhile investment with little downside risk.

2. They trusted their friend’s ‘hot tip’ and dived head first without weighing all the costs and benefits that the investment might bring. They assumed that if it were a good investment for their close friend, it was good for them too.

3. Best of all, they loved the NO MONEY DOWN proposition! The property sold by the developer came with 100% financing from a bank in Malaysia! Other than RM$5,000 administration fee and legal costs, they did not have to pay down the mortgage until the property is completed and rentals start rolling in.

They thought: why not own another property in addition to the one in Singapore? Things could not get any better than this. The property has a freehold title and is located in a middle-high end residential neighbourhood with a mall complete with all the necessary amenities: schools, nurseries, clinics, etc. and half an hour’s drive to Singapore.

Four years later, around mid-2018, the property was completed. The 15-year mortgage kicked-in on the RM$618,800 principal at 4.5% p.a. interest. They were repaying RM$5,000 a month to the bank.

During the 10 months, there were no calls looking to rent the apartment.

So it has been purely cash outflow, with maintenance expenses, property tax, utilities bills and of course the hefty mortgage.

This NO MONEY DOWN deal in Johor made matters worse for the family’s finances.

John’s parents have taken on 3 corporate loans for their family business. Liabilities due in the next 2 years amount to about S$380,000, i.e. regular payments of about S$16,000 each month. Amidst the slow business environment for engineering contractors in Singapore, their monthly cash flow for the business and family struggled to stay positive.

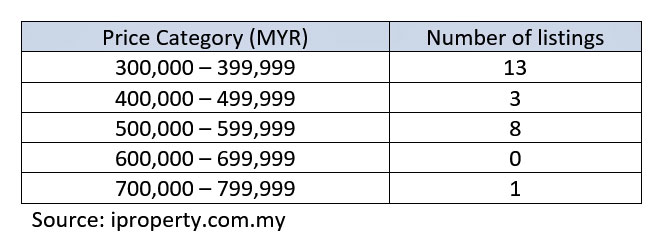

So how did their ‘brilliant’ investment opportunity fare to date? The initial price of the 3-bedroom apartment of 1,097 sqft was RM$618,800. A quick online survey of various property websites resulted in a few dozen listings which indicated an asking price range of RM$308,000-700,000. Half of the listings for similar-sized 3-bedroom units were below RM$440,000, with the lowest being RM$308,000 which was amongst a handful that were listed under “foreclosure sales”. There was a single listing at RM$700,000, a clear outlier as the next highest listing we could find was at RM$598,000.

Taking the top outlier out of the picture, the average market price of the two dozen listings was around RM$430,000. For John’s parents, assuming that they are able to divest the apartment at RM$430,000, they will suffer a capital loss of RM$188,800, or about 30%, over the past 5 years, excluding other costs.

This is a massive loss for a family who has barely enough money to tide through daily living expenses.

This capital loss will be further exacerbated by the fact that they have signed up a 100% Loan-to-Value (LTV) mortgage for the RM$618,800 investment. This loan has a fixed interest rate of 4.5% per annum. Over the 15-year loan tenure, the interest will cost about RM$230,000. Adding that to the principal sum, John’s parents would need to foot a massive RM$850,000 over the 15-year period.

Alternatively, John’s parents could decide to sell the property at the average market price today, they would still need to foot a loss of RM$188,800 plus interest expenses and legal costs. Since “no money” was put up at the start, even a slight decrease in value from the original amount of the property would give us a negative return on investment. What a way to beat the market.

Assuming that today’s market is indeed at RM$430,000, should John wait for the market to pick up, he would have to wait for Malaysia’s real estate market to rebound by 10% a year continuously for the next 5 years before he can breakeven on the investment. However, there do not seem to be many interested buyers at this price, which is why foreclosure sales are priced from a mere RM$308,000. If John had to divest at RM$308,000, the capital loss will be RM$310,800 before fees and expenses.

So, what went wrong? A deeper reflection on the entire picture will show us just how many and how deep the caveats are in such an ‘investment strategy’, as well as the lessons John learnt from this case.

1. If it’s too good to be true, then it probably is.

We hope that the age-old saying is not true. We always hope for a better life for our family. That hope makes us feel as if we have to outperform the market to get ‘out of the rat race’ and head towards ‘financial freedom’. But get-rich-quick schemes are never the solution. These are schemes that tap on our insecurities in the hope that we ignore all the ‘what-ifs’ that could get us into more financial troubles. ‘No money down’ property schemes are highly risky investments with too many what-ifs for investors. Even for highly experienced real estate investors such as REITs managers, the rules limit their gearing ratio a maximum of 45%.

2. Pick up a book (or go to your best friend, Google)

A major reason why many fall prey to such schemes or scams is due to the lack of research about the asset class they are investing in. Basing your research on a ‘gut feeling’ which many claim as their ‘keen acumen’, or a ‘hot tip’ from a friend or relative is obviously insufficient. Any investment of any kind requires good solid research to back up, both quantitative and qualitative. If you’re not sure, pay a trustworthy expert to do the due diligence for you. Read a book related to the asset class or simply google it! And do make sure that you check on the reliability of the sources too.

3. If at first you don’t succeed… err… try something else

It does not always have to be real estate. Good investments can be found in many areas around us. Invest in something you understand. If you can’t understand the asset class well enough, chances are it’s not a well-suited investment for you. Real estate as an asset class requires more than just betting that the market will go up or down in your favour. There is one revenue line and many lines of cost components involved in generating the overall returns that have to be considered. If that sounds too foreign for you, try investing in an asset class that’s a lot more understandable.

It would be foolish for one to think that he knows how to invest in real estate simply because he has lived in real estate his whole life.

Question: If you were caught in a similar situation, what might be your next steps?

Contributors:

Ku Swee Yong is a licensed property agent and the CEO of International Property Advisor Pte Ltd and Joel Kam is a future graduate of the Cass Business School from London, UK.