Finance

Six hidden costs of home renovation and how to avoid them

Renovating can be an exciting project that can transform your home. To make sure that you can end up with a beautiful new design without breaking the bank, we’ve highlighted a few costs that are often overlooked by homeowners as they plan to renovate.

Given the high cost of home renovations in Singapore, homeowners want to be sure that they don’t incur unnecessary expenses and aren’t surprised by additional costs once they finish renovating. In order to help these individuals, we’ve identified potentially costly issues that homeowners should be cognisant of before they decide to renovate.

Last Minute Changes

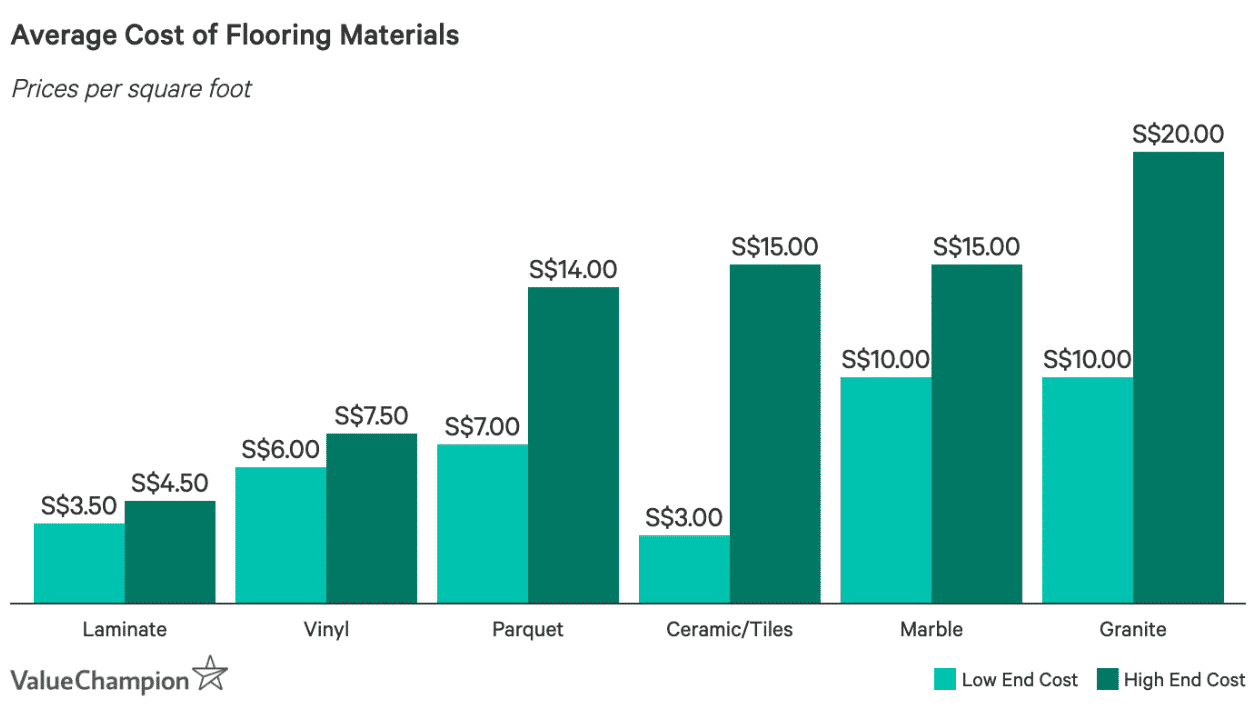

To the extent that it is possible, it is important to avoid making last minute changes to your renovation plans. Besides creating a headache for your contractor, you can increase the total cost of your project beyond its original quote. For example, a seemingly innocuous adjustment such as requesting a different type of flooring material can drive up the cost of your renovation.

For instance, choosing different materials, or even a different variant of the same material, can increase the cost of your renovation by hundreds of dollars. This problem can be easily avoided through proper planning and by sticking to your original plans.

Sometimes the changes may be outside of your control. Unfortunately, in this case you may not be able to avoid paying the higher cost. For example, your desired materials could be out of stock, or you may find out too late that what you ordered doesn’t fit in your original design or may not be up to par with your expectations.

To avoid these instances, you should make sure you have an open line of communication with your contractor and ensure the quality and availability of the materials as early as possible to avoid ending up paying significantly more for expensive alternative materials.

Forgetting to Take Measurements

As simple as it sounds, forgetting to take measurements before you purchase furniture, fixtures or appliances can be a costly mistake. In some cases, you will be able to simply return these items; however, sometimes you will have to pay additional shipping fees or even buy brand new items to fit your renovation needs.

For these reasons, it is important to take the time to double-check all of these minor details before you make purchases related to your project.

Accidental Damages

Unfortunately, when renovation accidents happen, they can be expensive to fix. Fortunately, those caused by your contractor are not likely to be an added cost for you, though they may delay the entire process. However, any damages that you cause during your own efforts to the renovations can raise the cost of your total bill. Furthermore, damages caused by your renovation project are usually not covered by home insurance.

While damages that occur during renovation are not typically covered by your homeowners insurance, damages to the renovations made in your home that occur following your renovation should be covered. For this reason, it is important to insure yourself with the best home insurance for your home in order to protect your recently completed renovation project.

Finding a Place to Stay

Smaller renovations may not require you to leave your home; however, larger projects may require that you find another place to stay. Staying a few nights at a hotel can cost hundreds of dollars, and longer-term situations may require that you find a short-term rental, which could cost even more.

Similarly, if you end up staying in your home during the renovation, you may end up up eating out more if your kitchen appliances are affected by the project.

Homeowners may not think about these costs as they plan their renovations, but should add to food and lodging to their budget if their project requires them to leave their home and they do not have alternative options, such as staying with friends or family.

Getting the Wrong Renovation Loan

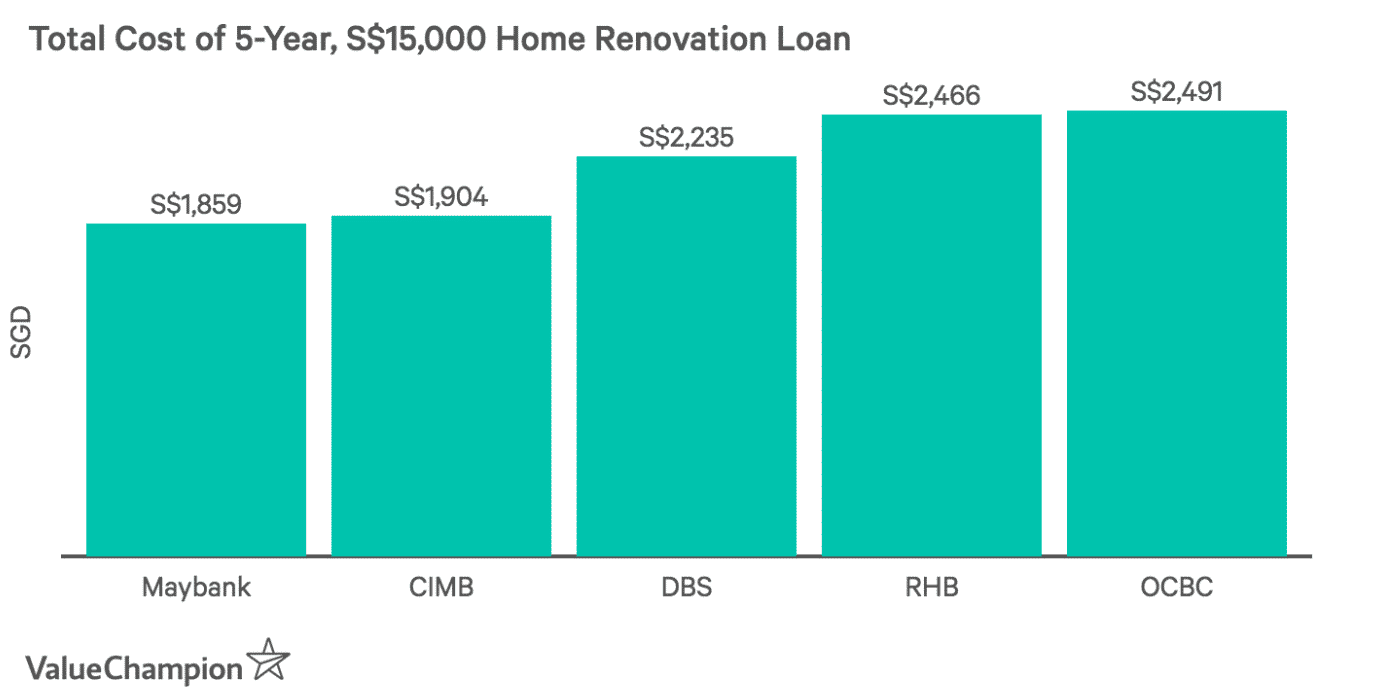

Many of those seeking to renovate their home will not have the ability to pay for the entire cost of their ideal renovation without using financing. However, getting the wrong renovation loan can significantly drive up the cost renovating.

After analysing the renovation loan offerings in Singapore, we found that the cheapest renovation loans can save borrowers approximately 14 – 28% compared to the average renovation loan. This means that choosing the wrong loan can cost hundreds or even thousands of dollars, which can substantially increase the cost of your renovation project.

Varying Fee Structures

If you have never renovated your home, you are likely to have never worked directly with a contractor. It is important to understand that not all contractors offer the same price structures, which can be tricky when you are trying to estimate your total bill.

For example, some do not add the cost of hauling demolition debris or the cost of cleaning upon the conclusion of the project in their quotes. This isn’t unheard of, so make sure you check with your contractor about these types of fees to avoid being blindsided.

Save Money by Planning Ahead

With all of the advice listed, it is important to be aware of potential pitfalls that can set you back financially. With this in mind, it is important to have agreed upon a clear plan with your contractor and considered how you would react depending on various contingencies. In the end, careful planning can help you avoid thousands of dollars in hidden costs associated with your home renovation.

This was first published at Value Champion’s website, “6 Hidden Costs of Home Renovation & How to Avoid Them“.