Opinion

The CPF and HDB ticking timebombs

by Brad Bowyer

The post on the comparison with Germany and Denmark sparked a lot of heated debate and brought one BIG and very worrying fact to the surface.

But first a clarification because a lot of people got lost in the comparison of EVERYTHING about Germany and Denmark and micro analysing figures, but this is unimportant in the BIG PICTURE.

The BIG PICTURE summary.

1. Germany has a pension fund slightly smaller than ours and whatever other challenges it has it gives a reasonable pension to over 20 million people whereas we fail to give a basic one to less than 1 million

2. Denmark, a country of similar population to ours, and again regardless of anything else, and with a much smaller fund gives a very good pension indeed to its people.

There is probably a happy medium of fund size and payouts between those 2 points for a population of our size that would generate a very decent sustainable pension for all however under our current model it won’t be found.

Because as was discussed by many yesterday we don’t run our CPF like any other pension fund as it gets chopped up in to buckets with medisave, has the minefield of private investment withdrawal options, education expenses withdrawal options and of course mandatory expensive but poor cover insurance policies and the biggie HOUSING.

This use in housing is only matched in its damage by the extremely low interest rates paid on our funds which nullifies much of the compounding effect and being below inflation guarantees a reduction in spending power of our savings even without the housing drain.

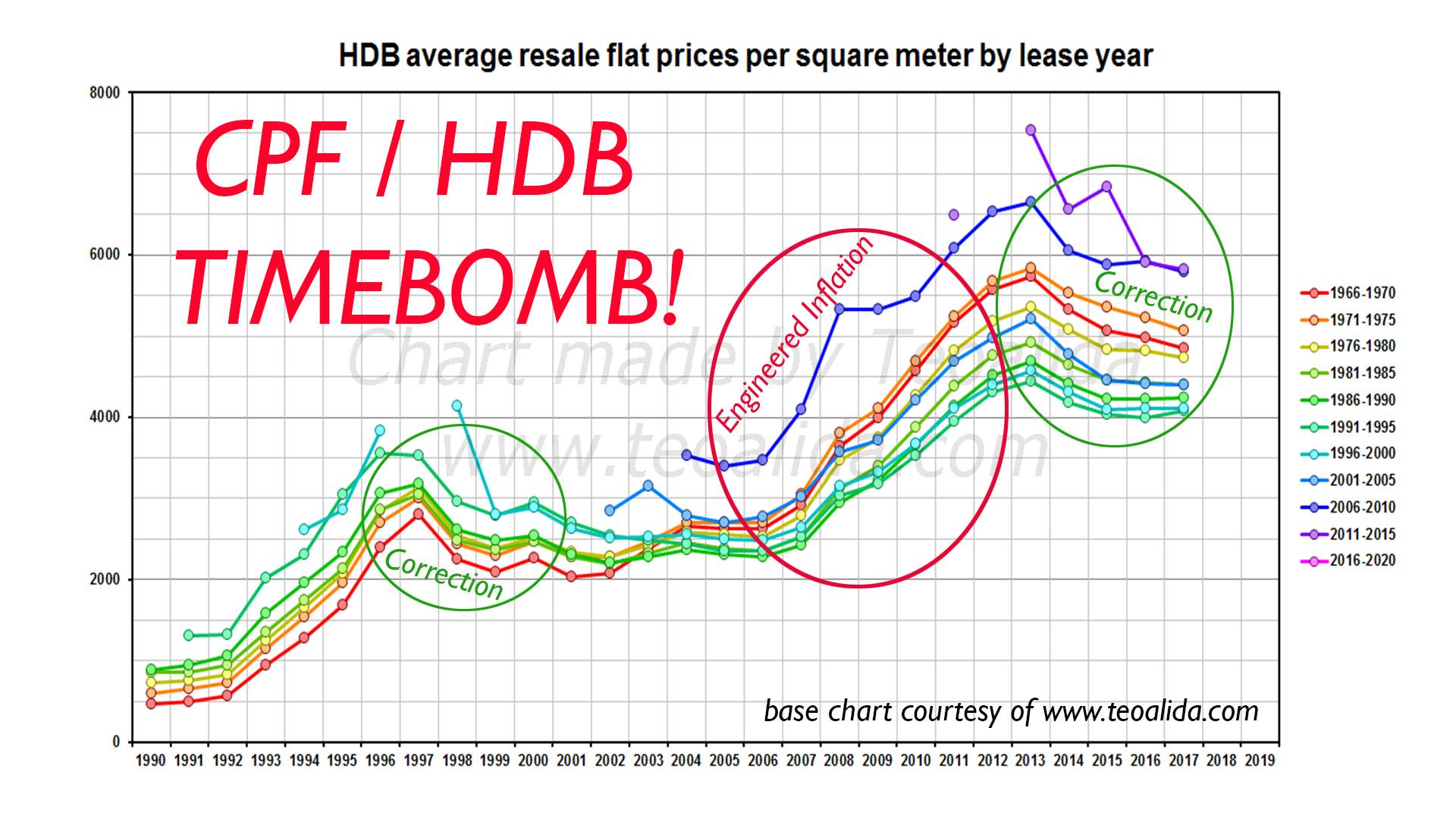

Now to the housing part. In a Q&A with Mano Sabnani he pointed out an error I made when I mistakenly read a CPF headline number. I thank him for that as he helped me clarify that we actually have SGD$216.9B of our CPF funds tied in our properties, that’s 63.66% of it. SGD$146.2B or 42.92% in HDB housing.

With so much of our savings in 1 bucket we are opening ourselves up to a world of hurt and now we can understand more why PAP policies in the 2000s appeared to be very focused on artificially inflating the prices of HDBs by reducing new supply and driving and talking up the prices but what happens when reality hits?

You buy your HDB high and can only sell it low, if you can find a buyer, or do a low lease buy back direct from HDB. Either way you have a big loss, no home and what should have been your savings compounded over time evaporating and leaving you with little to no retirement.

While there is still money in our national pot, we need to look really closely at what has happened to our funds, what is the true value of an HDB, why are interest returns on CPF so low and how do we redress this mess.

As the fund size example of yesterday shows we can fix it if we can reorganize our funds and start using them professionally to industry and peer standards. Here our small size will help as we don’t have to care for 80 million plus Germans only 3.5 million plus Singaporeans.

What we should also ask is being the problems architect is the PAP the team to fix it?

This was first published on Brad Bowyer’s Facebook page and reproduced with permission.