Current Affairs

Achieving sustainable financial freedom: What works and what doesn’t

By Property Soul / Article posted on 16th June (Monday)

It is OGIM (Oh God It’s Monday) again!

You somehow manage to drag yourself out of bed and leave home in a hurry. You squeeze into an overcrowded train, praying that the MRT lines won’t have Monday blues like you. Or you drive turtle speed on the highway that takes forever to reach the office.

You sit in front of the computer with your mind completely blank, wondering how to survive that sales meeting coming up next. You suddenly recall today is the deadline for a big project. Yet a demanding customer chooses to call you the first thing in the morning to lodge a complaint. Your nightmare boss says he needs to see you immediately …

Sacrificing happiness for comfort

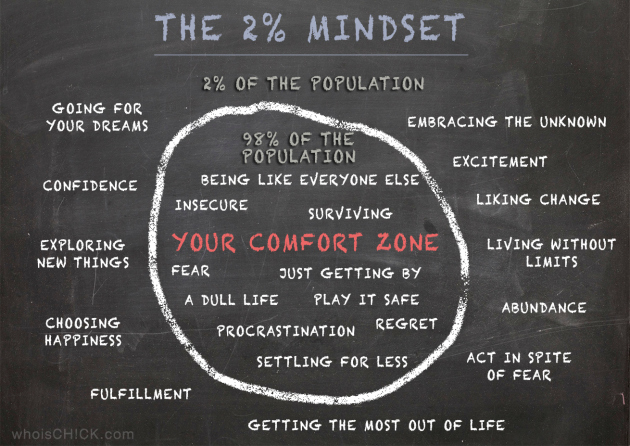

Whoischick.com points out the fact that we can choose to be in two areas in our everyday life: the comfort zone or discomfort zone.

- Comfort zone: 98% of us are being like everyone else. We live with insecurity, fear and regret. We procrastinate, play it safe, settle for less and lead a dull life. Most of the time we are just surviving or getting by.

- Discomfort zone: Only 2% of the population are living their dreams. They have chosen happiness and living without limits. They have confidence, dare to explore new things, embrace the unknown and act in spite of fear. They are looking for changes, excitement, abundance and fulfillment. They believe in getting the most out of life.

What about you? Are you living the life you really like? Do you have the guts to live the life you always want?

A comfort zone does not equal to a safe zone

But this is easier said than done.

Everybody wants the freedom to do the things they like. But the moment you stop tolling all day in the office, how do you pay the bills at the end of the month? Who is going to support your family? How can you save for your retirement?

You can choose to stay in your comfort zone. But a comfort zone is not necessarily a safe zone. Company downsizing and retrenchment sometimes have nothing to do with whether you have met your KPIs or sales quota, how much past contributions you have made, or how serious your OGIM symptoms are.

Facing regular restructuring announcements in my corporate life, it was imminent for me to have a contingency plan. My Plan B was buying some good properties that could continuously generate passive income for me. If one day my name was in that batch of employees to let go, my tenants would help to pay my bills.

I also started researching about possible ways to achieve financial freedom. It is not about not having to work at all, but more about the freedom of choosing to do the type of work I enjoy, the liberty to spend my time the way I prefer, etc.

Throughout the years, I have seen many people who try different ways to realize their dream of being financially free. Some work while some flop.

Financial freedom: what don’t work

Some people may claim that they ‘have been there’. However, if their financial freedom is not sustainable, and they eventually go back to where they were, I won’t call that a proven strategy at all. These methods include:

- Following any get-rich-quick program that guarantees to make you a millionaire but sounds too good to be true.

- Joining any high risk ponzi investment scheme that promises high return in a short period of time. No such scheme can stand the test of time in our past history.

- Winning the lottery, striking the jackpot or reaping a windfall at the casino that you will quickly spend or lose them all and go back to square one in no time.

- Receiving a sudden big inheritance or donation with no prior training in personal financial management or investment. Think the woman who spent her $1 million donation after the horrible accident of her husband, all in barely one year’s time.

Financial freedom: what work

Below are three proven methods to achieve financial freedom that I have found to be sustainable in the long term.

- Investing in good stocks or good properties that becomes a stable stream of income in terms of dividends or rental return, and promises a sizable capital gain when cashing out one day.

- Building a solid and sustainable business that offers a reliable source of income in the long term.

- Having a wealthy spouse who has high earning power or the financial means to support your lifestyle, and is generous to you (note: to you only).

It is good to be able to achieve one of the above. But it is best to attain all of them if you know what I mean!

This article was first published in PropertySoul.com