Commentaries

MediShield Life: Premiums up 100% after transitional subsidies?

By SY Lee and Leong Sze Hian / Image from Ministry of Health

MediShield Life – everything also increase?

We refer to the article “Enhanced benefits proposed for MediShield Life” (Today, Jun 6).

The article reports that there will be substantial increases in benefits for MediShield Life that will cover all Singaporeans for large hospital bills.

- Many of the claim limits will go up

- Outpatient cancer chemotherapy and radiotherapy treatments could also have higher claim limits, as could surgical procedures.

- Under MediShield Life, nearly six in 10 B2 and C Class patients with large bills exceeding S$10,000 will pay less than S$3,000, in Medisave and cash, from only one in 10 today.

- Coverage will also be extended to those aged above 90 or with pre-existing conditions.

- The Government will provide subsidies for the bottom two-thirds of households here, as well as transitional subsidies for the first four years of MediShield Life.

It is stated in the article that the MediShield Life Review Committee (chaired by Mr Bobby Chin) has recommended to raise claim limits and reduce co-insurance rates, as well as leave deductibles untouched.

“All three elements have significant impact on premium levels, said Mr Chin. Many people said they preferred to protect themselves against very large bills, which would be addressed by lower co-insurance and higher claim limits.”

“They also preferred to pay lower premiums on a regular basis, rather than lower deductibles, which would be felt only if they are hospitalised.”

The committee is recommending for those with pre-existing conditions to pay 30 per cent more in premiums for 10 years. Other policyholders will pay no more than 3 per cent from current premiums for the purpose of bringing those with pre-existing conditions into MediShield Life.

It is reported that the Government will bear the bulk of costs of universal coverage.

Another reason given for the need for higher premiums is the need to pay more while one is still working to keep premiums affordable in old age.

However with all the promising recommendations made by the MediShield Life Review Committee, the following questions remain unanswered:

Medishield scheme accumulated surpluses?

What is the accumulated surplus plus interest since the MediShield scheme has had annual surpluses since its inception? About $1 billion? (See more here)

Still not spending any money on healthcare?

From a cashflow perspective, will the Government still not be spending a single cent on healthcare because Medisave contributions in a year may continue to exceed all withdrawals including government healthcare spending?

Are there any countries in the world that operate their healthcare system like this?

After transitional subsidies – premiums increase more than 100%?

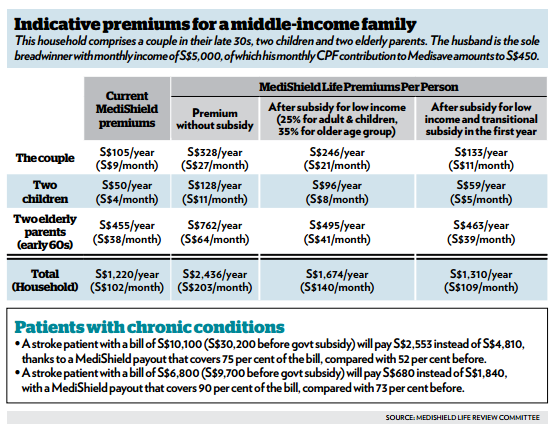

(Table as shown in the Today newspapers)

The problem with transitional subsidies may be that according to the example given in the subject news report – for a family – their annual premiums will increase from $1,220 to $2,436 if they do not qualify for the “subsidy for low income”.

This is an increase of 100% in the family’s annual premium for their healthcare insurance.

No projections into the future?

And we have not even factored in or projected how much the increase will be as the couple in their 30s and their 2 elderly patents (early 60s) get older, as premiums may generally increase with age?

Why are such projections not mentioned at all in the media report?

Correction note – The figures “1 Trillion” has been corrected to “1 Billion”